Abstract

This paper examines the effects of the COVID-19 pandemic on CDS, stock returns, and economic activity in the US and the five European countries that have been most affected: the UK, Germany, France, Italy, and Spain. The sample period covers the period from 11 March 2020 to 19 February 2021. In the empirical analysis, first, we estimate benchmark linear VAR models and then, given the evidence of parameter instability, TVP-VAR models with stochastic volatility, which are ideally suited to capturing the changing dynamics in both financial markets and the real economy. The linear VAR responses of CDS to the number of COVID-19 cases are positive and statistically significant, whilst those of electricity consumption are insignificant and those of stock returns vary across countries in terms of their sign and significance. The results from the TVP-VAR analysis indicate that the effects of shocks on the system variables was more pronounced during the initial stages of the pandemic and then decreased in the following months. Specifically, there was a positive impact of the number of COVID-19 cases on CDS and a negative one on stock returns and economic activity, the latter two being interlinked.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The COVID-19 outbreak started with the reporting to the World Health Organization (WHO) on the last day of 2019 of pneumonia cases of unknown cause in Wuhan, Hubei province of China. The WHO declared a Public Health Emergency of International Concern on January 30, 2020, after the virus was found to be transmitted from human to human and was also detected outside China (WHO 2020a). Because of the international spread and alarming levels of COVID-19 cases, as well as the inertia of policymakers, the WHO classified the COVID-19 outbreak as a global pandemic on March 11, 2020 (WHO 2020b). As of August 18, 2021, the number of confirmed COVID-19 cases had surpassed 200 million, with over 4 million deaths in the world as a whole (WHO 2021) and devastating effects on public health, the real economy and financial markets.

Following the easing of trade tensions between the US and China, investor sentiment had been bullish in late 2019 but quickly became bearish in early 2020 when increasing evidence of the global spread of the coronavirus drastically changed positioning and pricing in the international financial markets (BIS 2020; FSB 2020). Owing to the higher degree of uncertainty, investors rushed to purchase safe and liquid assets, which led to sharp declines in stock market indices (IMF 2020). Specifically, stocks in the US and euro area lost around 35% of their value between February 19 and March 23 (Ampudia et al. 2020). The S&P 500 fell by 20% from its previous peak in just 16 trading sessions (IMF 2020), and 18 stock market jumps occurred in the 22 trading sessions between February 24 and March 24, despite the mortality rate being much lower than during the Spanish Flu, when there was no single daily stock market jump (Baker et al. 2020).Footnote 1

The COVID-19 pandemic also had real effects, both on the supply and demand side. Workers reduced their labour supply, consumers were reluctant to spend, and the containment measures aimed at saving human lives had further negative effects on economic activity (Eichenbaum et al. 2021). All these factors combined resulted in the worst global recession since the Great Depression of 1929 (Gopinath 2020). The International Monetary Fund (IMF) and the World Bank (WB) respectively estimated that the global economy contracted by 3.3% and 4.3% in 2020 (IMF 2020; World Bank 2021).

It is well known that economies and stock markets respond to political and geopolitical events (Chau et al. 2014; Al‐Maadid et al. 2021; Elsayed and Helmi 2021), terrorist attacks (Chesney et al. 2011; Phan et al. 2021), and natural disasters (Cavallo and Noy 2011; Horvath 2021). There is less evidence on the impact of pandemics, which are relatively rare compared to other types of events and whose effects are often confined to specific regions. However, the global nature of the COVID-19 pandemic made it immediately apparent that both the world economy and financial markets would be severely affected (Al-Awadhi et al. 2020; Sharif et al. 2020; Alomari et al. 2022).

The present paper aims to provide extensive evidence on the effects of the COVID-19 pandemic on stock returns, CDS, and economic activity in the US and five European countries (the UK, Germany, France, Italy, and Spain) which have been among the hardest hit developed economies. In addition to benchmark linear VAR models it uses a time-varying parameter vector autoregressive (TVP-VAR) one with stochastic volatility to capture the evolution over time of financial and economic variables during the various phases of the pandemic. The chosen approach is the most appropriate for our purposes (Primiceri 2005; Koop et al. 2009; Caporale et al. 2020; Nakajima 2011) given the fact that the COVID-19 pandemic had different waves following the initial outbreak.

The layout of the paper is as follows. Section 2 provides a brief review of the relevant literature. Section 3 describes the data and the TVP-VAR methodology. Section 4 discusses the empirical findings. Section 5 offers some concluding remarks.

2 Literature review

Following the COVID-19 outbreak, various studies have been carried out to analyze its consequences for financial markets. Most of them have focused on the impact of COVID-19 cases and deaths on stock markets. For instance, Al-Awadhi et al. (2020) investigated the effects of COVID-19 on the Chinese stock market from January 10 to March 16, 2020, and discovered that the daily growth rate of total cases and total deaths had a negative impact on stock returns in all sectors. Ashraf (2020a) examined the impact on stock markets of daily COVID-19 cases and deaths in 64 countries between January 22 and April 17, 2020, and reported that the former had a stronger effect and that there was evidence of time variation. Haroon and Rizvi (2020) concluded that the increasing number of COVID-19 cases had reduced liquidity in emerging equity markets during the period from January 1 to April 30, 2020. Xu (2021) explored the effects of COVID-19 on the US and Canadian stock markets from the initial outbreak to July 2, 2020, and found a less pronounced negative effect in the case of the former country. Al-Quadah and Houcine (2022) examined the impact of daily confirmed cases on stock returns in the six countries most affected by the pandemic in their geographical area between 1 March and 1 August 2020. They reported that the negative reaction of stock markets was strong in the early stages of the pandemic. Exploring 21 emerging markets between 22 January and 21 December 2020, Guven et al. (2022) showed that the daily growth in cases and deaths had a negative impact on stock returns, which was mitigated by government COVID-19 related restrictive policies. Analyzing the six most affected countries up to 24 September 2020, Ganie et al. (2022) concluded that COVID-19 cases caused a sharp decline in stock returns in the Spring of 2020, which was followed by a recovery, especially in the US and India, towards the end of the sample. Amin et al. (2022) found that the number of COVID-19 cases had negative effects on stock indices in the 12 countries of the American peninsula from 10 March to 9 April 2020. Investigating the period from 21 January 2020 to 10 August 2021, Yilmazkuday (2023) found that higher daily cases pushed down the S&P 500 index, though this effect weakened over time.

Another strand of the literature employed various proxies to analyze the impact of the pandemic on the stock markets. Ambros et al. (2021) concluded that COVID-19 news increased volatility in eight major European stock markets between January 1 and March 31, 2020. Chundakkadan and Nedumparambil (2021) analyzed investor sentiment using benchmark stock market indices for 59 countries as well as the Google Search Volume Index over the period from February 1 to April 30, 2020; they found an inverse relationship between the research volume of pandemic news and daily stock returns. Alomari et al. (2022) examine the relationship between changes in the newspaper-based infectious diseases tracking index (ITI) and sectoral stock market returns in the US. They found that the inclusion of the COVID-19 period in their sample data confirms a stronger relationship across all industries. However, the relationship between the ITI and returns is asymmetric across different market conditions for the technology, industrial, healthcare, and consumer staples industries. Szczygielski et al. (2022) provided evidence that COVID-19 related uncertainty decreased returns and increased volatility in a sample of 68 global industries. Cervantes et al. (2022) showed that panic indices explain stock market deteriorations in advanced and emerging markets between mid-January 2020 and mid-February 2022.

Some explored the impact on stock markets of the restrictive measures adopted by governments to contain the spread of the virus. D’Orazio and Dirks (2020) showed that lockdown policies had substantial adverse effects on stock market indices in the eurozone during the period from January 1 to May 17, 2020. Aggarwal et al. (2021) found that between December 2019 and May 2020, lockdowns affected stock returns in 12 countries negatively through market risk premiums and positively through growth projections. Analyzing 42 countries between 22 January 22 and 20 May 2020, Scherf et al. (2022) showed that stock markets responded negatively to lockdown restrictions and provided evidence that they underreacted during announcements and overreacted in the following days. Klose and Tillmann (2023) demonstrated that lockdown announcements affected negatively stock markets in 29 European countries in 2020 and 2021. Carrying out an event study from 23 April 2019 to 17 April 2020, Ji et al. (2024) reported that the response of stock markets to the lockdown measures was negative and rapid in 13 global stock markets. By contrast, Saif-Alyousfi (2022) found a positive relationship between containment measures and stock returns between 1 January 2020, and 10 May 2021 in a panel of 88 countries.

Other studies report that the initial negative effects on stock markets subsequently disappeared. For instance, Capelle-Blancard and Desroziers (2020) found that 79 stock markets were no longer affected by the number of COVID-19 cases between March 23 and April 30, 2020. Topcu and Gulal (2020) showed that the negative effect of COVID-19 on stock markets had decreased gradually and had tapered off by mid-April 2020 in 26 emerging market economies. Anh and Gan (2021) found that in Vietnam, negative stock return responses to COVID-19 turned positive in the lockdown period between April 1 and April 15, 2020. Harjoto and Rossi (2023) also said that the stock market recovered faster during the COVID-19 pandemic for both emerging and developed economies. Aldhamari et al. (2023) found that the impact of stringency measures on stock returns in Malaysia was negative, but these recovered following the adoption of stimulus packages.

One of the main reasons for this rebound is the massive monetary expansion and fiscal stimulus packages announced at the national and international levels since mid-March 2020. Ashraf (2020b) found that income support announcements had a positive impact on stock returns in 77 countries from January 22 to April 17, 2020. Klose and Tillmann (2021) analyzed the impact of monetary and fiscal policy announcements on financial markets in 29 European countries during the period from February 17 to April 24, 2020. They reported that those concerning asset purchase programs led to higher stock returns, while those about fiscal stimulus packages resulted in lower stock prices. Chang et al. (2021) showed that income support packages and other fiscal measures increased stock returns in 20 countries between January 2 and July 21, 2020. Narayan et al. (2021) concluded that stimulus packages introduced in March 2020 positively affected stock returns in Canada, the UK, and the US between July 1, 2019, and April 16, 2020. Cortes et al. (2022) examined spillover effects of the Fed’s unconventional monetary policies during the global financial crisis (GFC) and the COVID–19 pandemic and found that they were negative in the former case and positive in the latter. By contrast, Pham and Chu (2024) showed that economic stimulus packages caused a decline in stock returns in 14 countries between December 2020 and January 2022.

The pandemic also had significant adverse effects on economic activity, especially in the spring of 2020, when national lockdowns were imposed widely. Several studies have investigated such effects on the real economy using different proxies as real-time indicators and confirmed the sharp drop in economic activity. Chen et al. (2020) analyzed the impact of COVID-19 on economic activity in Europe and the US from January to May 2020 using several high-frequency indicators such as unemployment insurance claims, electricity consumption, and the Google Community Mobility Index; they reported significant contractions prior to the adoption of economic support policies. Using the Baltic dry index as a proxy for economic activity from 21 January to 26 February 2021, Hasan et al. (2021) concluded that COVID-19 cases reduce economic activity, but the impact is short-lived. Carvalho et al. (2021) analyzed transaction data via BBVA in Spain from 1 January 2019 to 29 June 2020. They showed that expenditure growth (year-on-year) decreased by around 60% when a nationwide lockdown was announced in mid-March 2020. Lewis et al. (2022) investigated the early effects of the pandemic in the US up to 2 January 2021 using a weekly economic index (WEI); they found that the decline in economic activity started in the week ending on 21 March and that there was a further slump in the week of 25 April, with an 11.45% drop in the WEI. Employing various indicators, such as flights, nitrogen dioxide emissions, and energy consumption, Deb et al. (2022) showed that stringency measures significantly and negatively affected economic activity, a 10% drop in industrial production occurring in the 30 days following their implementation. Angelov and Waldenström (2023) used firms’ tax-registration data in Sweden until March 2021. They reported that the COVID-19 pandemic led to a fall in economic activity due to declining tax revenues and firm turnover. Beyer et al. (2023) reported that nighttime light intensity decreased between May and July 2020 in India, which may imply a decline in GDP around 6%. Unlike previous studies, Gagnon et al. (2023) measured the impact of COVID-19 on economic activity by directly analyzing the determinants of real GDP. They reported that the impact of COVID-19 deaths on GDP growth was much lower than that of the containment measures, especially in low-income countries.

Electricity consumption is one of the most used proxies to gauge the economic impact of the COVID-19 pandemic. Many studies showed that electricity consumption declined when containment measures were imposed (Abu-Rayash and Dincer 2020; Bahmanyar et al. 2020; Bento et al. 2021; Santiago et al. 2021; Wang et al. 2021; Wen et al. 2022; Yukseltan et al. 2022), especially in the case of firms (Sánchez-López et al. 2022; Bover et al. 2023). Some studies have also quantified the impact of lower electricity consumption on economic activity. Fezzi and Fanghella (2020) examined daily electricity load data in Italy from January 1 to June 30, 2020, and found that the three weeks of strictest lockdown in March and April led to output losses of approximately 30% of GDP. Janzen and Radulescu (2020) estimated that the 4.6% decrease in electricity consumption during the lockdown in Switzerland corresponded to a 7% decline in output. Using electricity consumption, Fezzi and Fanghella (2021) provided evidence of severe GDP losses in 12 European countries in the first wave of the pandemic. Beyer et al. (2021) found that the negative growth effect of the decline in electricity consumption in India in the second quarter of 2020 was 20.8%. Analyzing data for Huban province, China, from 1 December 2019 to 31 March 2020, Ai et al. (2022) reported that electricity consumption declined by 27.8% from the beginning of the pandemic, which implies a loss of 121.187 billion yuan. Arshad and Beyer (2023) found that the decrease in electricity consumption in Bangladesh and Dhaka in April and June 2020 caused 8% and 17% GDP losses, respectively.

Several studies have examined the effects of the COVID-19 pandemic on sovereign credit spreads. Using an event study approach, Andrieş et al. (2021) provided evidence of abnormal changes in CDS in Europe during the pandemic. Daehler et al. (2021) concluded that the higher mortality rate during the pandemic increased CDS spreads. Analyzing data for 78 countries from 2 January to 31 August 2020, Pan et al. (2021) showed that an increase of 1% in COVID-19 cases led to a rise of 0.17% in sovereign CDS. Augustin et al. (2022) concluded that in a sample of 30 advanced economies, sovereign credit spreads responded positively to country-specific daily increases in COVID-19 infections. Hao et al. (2022) investigated the impact of the COVID-19 shock on sovereign credit risk for 40 developing and advanced countries from 1 January 2019 to 30 November 2020. They found that this increased CDS spreads, its impact being greater on short-term spreads. Kanno (2024) showed that the pandemic-related fiscal stimuli and new COVID-19 deaths increased sovereign CDS for 12 countries, including the G7 countries, in 2020.

By contrast, Cevik and Öztürkkal (2021) concluded that the pandemic had no significant effects on CDS when controlling for both institutional and macroeconomic factors in a panel of 77 advanced and developing countries. The adverse impact was significant only at the beginning of the pandemic, when containment measures appeared to lower sovereign CDS. Yıldırım Karaman (2022) reported that the COVID-19 shock increased CDS in Spain, Italy, and Portugal, while its impact was statistically insignificant in France, Germany, the Netherlands, Belgium, and Austria. Finally, Havlik et al. (2022) showed that monetary announcements had a greater impact than fiscal ones and reduced the spreads in the euro area during the COVID-19 pandemic.

Despite the COVID-19 pandemic being over as a public health emergency (WHO 2023), studies are still being carried out to understand its economic consequences. The present one contributes this area of the literature by providing a more comprehensive set of results concerning the time-varying responses of CDS, stock market, and economic activity to the pandemic in the US and European countries.

3 Data and methodology

3.1 Data

We employ daily data for the US and the five European countries most affected by the pandemic, i.e., the UK, Germany, France, Italy, and Spain, to investigate the impact of COVID-19 on stock returns, CDS, and economic activity. The sample covers the period from 11 March 2020, when the pandemic was declared by the WHO, to 19 February 2021. It includes two major waves of the pandemic, starting in the Spring and Fall of 2020. During this period, several lockdowns and intense restrictive government measures were implemented to slow down the spread rate (Roth et al. 2024). These measures provided partial control but also caused considerable losses in economic activity (Kok 2020; Furceri et al. 2021; Deb et al. 2022; Janzen and Radulescu 2022; Chen and Tillmann 2023; Matei 2023; Ma et al. 2023; Zou et al. 2024) and a decline in stock returns (D’Orazio and Dirks 2020; Aggarwal et al. 2021; Scherf et al. 2022; Klose and Tillmann 2023; Ji et al. 2024). Therefore, in order to take into account the impact of the containment measures we include in the model a stringency index as a control variable. The vector of endogenous variables for the estimated TVP-VAR model is defined as follows:

where \(case_t\) indicates the cumulative number of confirmed COVID-19 cases,\(str_t\) is the stringency index (the index takes values from 0 to 100, higher values corresponding to tighter restrictions), \(cds_t\) is the CDS spread on 5-year senior bonds, measured in basis points (increases in this variable could reflect a higher default risk caused by the greater economic uncertainty generated by the pandemic), \(ret_t\) denotes the stock market index of each country.

In this paper, the key variable used as a proxy for economic activity is daily electricity consumption, denoted by \(ec_t\) measured as the average hourly electricity load in megawatts.Footnote 2 A variety of factors can explain why electricity is used as a measure of economic activity. First, it should be noted that the most common measures of economic activity (such as the GDP and the industrial production index) are only available with monthly or quarterly frequency with significant delays. As a result, other indicators with a higher frequency of occurrence and shorter publication lags (Beyer et al. 2021) may be preferable. Second, there is a large empirical literature demonstrating the existence of a link between electricity consumption and economic growth (Narayan et al. 2008; Yoo and Kwak 2010; Sarwar et al. 2017).Footnote 3 Various studies have already employed electricity consumption to examine the impact of COVID-19 on economic activity (see, e.g., Chen et al. 2020; Fezzi and Fanghella 2020, 2021; Janzen and Radulescu 2020; Beyer 2021; Ai et al. 2022; Arshad and Beyer 2023) and some have shown that this variable is a good proxy for real-time tracking of economic activity indicators, such as GDP and industrial production (Fezzi and Fanghella 2021; Menezes et al. 2022; Galdi et al. 2023). Therefore, in this study, we employ daily electricity consumption to examine the real effects of the pandemic.

Concerning the data sources, note that the electricity load data have been taken from the European Network of Transmission System Operators for ElectricityFootnote 4 and the US Energy Information Administration.Footnote 5 COVID-19 cases, the stringency index, CDS spreads, and stock returns have been retrieved instead from the Thomson Reuters DataStream database (Refinitiv Eikon Datastream 2021). Since all variables exhibit a unit root, we take the first differences in their logarithms prior to estimating the TVP-VAR model.Footnote 6

The ordering of the variables in a VAR (Vector Autoregression) model is a crucial issue that reflects economic reasoning and the causal relationships between them. It determines how shocks to one variable affect the others in the system. The number of COVID-19 cases is placed first because the pandemic was an exogenous shock that influenced all other variables in the system. The next variable is the stringency index, which captures the restrictive measures adopted to contain the spread of COVID-19 and affects macro-financial variables. The third variable, CDS spreads, is affected by risk perceptions related to the pandemic. The fourth variable, stock returns, reflects the investors’ reactions to the pandemic and changing credit risk. Finally, economic activity responds to all previous shocks since it is affected by both pandemic-related policies and financial developments.

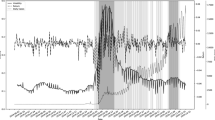

Before proceeding to the empirical analysis, the electricity consumption and stock price indices of the countries under consideration are plotted in Fig. 1. A visual inspection of the variable implies that economic activity and stock markets did not show stable behavior during the COVID-19 pandemic. The WHO identified two main global waves starting in the Spring and Fall of 2020 on the basis of the number of confirmed cases. COVID-19 uncertainty and lockdowns caused sharp drops in stock markets and economic activity during the first wave; the easing of restrictions in June 2020 then led to a moderate recovery. Although the number of confirmed cases was much higher during the second compared to the first wave (around 70 million cases were recorded between October 2020 and February 2021 as opposed to 6 million between March and June 2020, WHO 2021), the impact on the real economy and stock markets was less pronounced in the former case.

Time series plots of electricity consumption and stock price indices. Notes The left axis shows electricity consumption, while the right axis is for the stock price index. Electricity consumption data is the average hourly electricity load measured in megawatts, and weekends are excluded for consistency with stock price index data

3.2 Methodology

This section briefly outlines the structure of the TVP-VAR model used to estimate the time-varying responses. As argued by Primiceri (2005) and Koop et al. (2009), this model has important advantages compared to other nonlinear specifications. First, in contrast with threshold models, it does not require a transition variable governing the behavior of the variables across the regimes. Second, time-varying parameters capture gradual changes in the relationship among the variables. Finally, the time-varying variance–covariance matrix of the error terms can account for the impact of unanticipated exogenous shocks.

The TVP-VAR model is based on the Bayesian estimation of state-space equations and consists of a measurement equation and state equations for the time-varying coefficients. The measurement equation is specified as follows (Nakajima 2011; Primiceri 2005):

where \(\xi_{it}\) and \(c_t\) are the time-varying coefficients and intercept terms, respectively. The error terms are assumed to follow a normal distribution with a zero mean and a time-varying variance–covariance matrix \({\Omega }_t\). In order to extract time-varying shocks, this matrix is decomposed into \({\Omega }_t = C_t^{ - 1} {\Sigma }_t \left( {{\text{C}}_t^{ - 1} } \right){\prime}\) through a Cholesky decomposition based on a recursive ordering of the variables. The matrix, \(C_t^{\,}\), which measures the simultaneous relationship among variables, is a lower-triangular one, whereas \({\Sigma }_t\) is a diagonal matrix reflecting the time-varying idiosyncratic shocks:

Once the time-varying shocks have been identified, the model in Eq. (2) can be reformulated through a Kronecker product conversion, as outlined by Nakajima and Watanabe (2011):

To estimate the above equation, the time-varying parameters and error variances must be modelled; specifically, the following state equations are assumed to govern their behavior:

The equations \(\beta_{t + 1}\) and \(\delta_{t + 1}\) imply that the parameters of the measurement equation \(\beta\) and \(C_t\) matrix governing the impact of instantaneous shocks follow a random walk without an intercept.Footnote 7 In the equation for the standard deviations of the residuals, a geometric (exponential) random walk is employed, similar to the ARCH specification in the financial econometrics literature, where the estimated time-varying variances are placed on the diagonals of \(H_t\).Footnote 8 Furthermore, the error terms of the equations above are assumed to be independent of one another and to follow the normal distribution. It should be noted that a dummy variable for the lockdown periods would have been appropriate in a linear framework. By contrast, the TVP-VAR model does not require the inclusion of such a variable since it can capture both temporary and permanent shifts given the fact that the parameters follow a first-order random walk over time (Nakajima 2011).

4 Empirical results

4.1 Linear VAR results

Before analyzing the TVP-VAR models, benchmark linear VAR models are estimated. The cumulative responses of electricity consumption, CDS, and stock returns to COVID-19 case shocks are shown in Fig. 2. We first examine the effects of a one-standard-deviation shock to the number of COVID-19 cases on the stringency index. The responses of the latter are positive, but their significance differs across the countries. They are significant in all periods in the US and Germany and after the third period in the UK, Germany, and Spain. In Italy, the response is also positive but statistically insignificant at all time horizons. The impact of shocks on the sovereign risk of countries are presented in panel (b) of Fig. 2. The responses in France, Italy, and Spain are consistently insignificant across all time horizons. However, in the other countries, they are both positive and significant for some time horizons. Specifically, statistically significant responses are obtained after the third period for the US and the UK, and from the fifth to the seventh periods for Germany.

Linear VAR responses to COVID-19 case shocks. a Cumulative responses of the stringency index to COVID-19 case shocks. b Cumulative responses of CDS to COVID-19 case shocks. c Cumulative responses of stock returns to COVID-19 case shocks. d Cumulative responses of electricity consumption to COVID-19 case shocks

The responses of stock returns to the one standard case shocks follow different trajectories for each country. They are statistically significant in some periods, except for the US, and positive. They are significant up to the second period in the UK and Germany, to the fifth, eighth, and sixth periods in France, Italy, and Spain, respectively. Finally, the responses of electricity consumption to the one-standard-deviation shock to COVID-19 cases are statistically insignificant.

4.2 TVP-VAR results

In this section, to motivate the estimation of a TVP-VAR model, we examine parameter constancy in the linear VAR model. To this end, we plot the recursive residuals of the time-invariant VARs along with their two standard error confidence intervals (see Fig. 7 in the “Appendix”). Recursive residual plots obtained from the estimation of the linear VAR model reveal the presence of parameter instability, as the recursive residuals mostly lie outside the confidence intervals, especially during the early months of the COVID-19 pandemic. It is well documented in the empirical literature that most macroeconomic variables are subject to structural changes, and hence, the assumption of constant parameters might not be valid (see Stock and Watson 1998). Therefore, Sims and Zha (2006) argue that the covariance matrices in VAR models should allow for time variation to account for the underlying relationship among the variables. The implication is that a linear approach is not suitable for analyzing the possible effects of the pandemic on stock markets, CDS and economic activity, and thus we proceed to estimate TVP-VAR models using the set of signal and transition equations described in the previous section.Footnote 9 This involves the estimation of several parameters which could result in over-parameterization and inconsistent estimates. To prevent this problem a Bayesian approach based on the Markov Chain Monte Carlo (MCMC) algorithm is used. Previous research (e.g., Primiceri 2005; Nakajima 2011) has shown that the Bayesian method minimizes the risk of parameter instability by specifying the prior probability densities of the coefficients before assessing their joint posterior distributions. Of the various sampling procedures employed in the estimation of Bayesian VARs, we choose the multi-move sampling one developed by Shephard and Pitt (1997) and Watanabe and Omori (2004) following Nakajima (2011); specifically, we draw samples of 50,000 from the posterior distribution to achieve convergence of the time-varying parameters in the signal equations and the transition equations. In addition, the first 5,000 samples are reserved for the convergence of the parameters. Unlike the other sampling methods, e.g. the Metropolis-within-Gibbs sampler applied by Primiceri (2005), the multi-move sampler does not require putting aside some initial observations to calibrate the starting values of the parameters, and thus the full sample can be used for the TVP-VAR estimation.

Upon confirming the stability of the estimates for each country, we compute time-varying responses based on the identifying shocks derived from the time-varying variance–covariance matrix in Eq. (3).Footnote 10 These are shown in Figs. 3, 4, 5, 6. Panel (a) in each figure displays the time-varying cumulative responses for the time horizons \(t = 0,{ }1,{ }2,{ }....,15\).Footnote 11 Such responses are entirely different from the time-invariant ones in that they require an additional dimension to plot them over time. Panel (b) shows instead, in each case, the accumulated responses over the fifteenth-day horizon, \(h = 15\), with two standard error confidence bands to evaluate their significance over the sample period.

Time-varying responses of stringency index to COVID-19 case shocks. a Time-varying cumulative responses. b Cumulative responses at h = 15 with \(\pm\) 2 standard error bands

Time-varying responses of CDS to COVID-19 case shocks. a Time-varying cumulative responses. b Cumulative responses at h = 15 with \(\pm\) 2 standard error bands

Time-varying responses of stock return to COVID-19 case shocks. a Time-varying cumulative responses. b Cumulative responses at h = 15 with \(\pm\) 2 standard error bands

As in the case of the linear impulse response analysis, we first analyze the time-varying responses of the stringency index to the COVID-19 case shocks (see Fig. 3). It can be seen that positive case shocks have a positive and statistically significant effect on the stringency indices of all countries in the early stages of the pandemic, when governments implemented measures such as stay-at-home requirements, school and workplace closings, and travel restrictions (Hale et al. 2021). Although the UK was criticized for its insufficient and slow reaction to COVID-19 after the first cases were reported (Gaskell et al. 2020; Cairney 2021), it has the highest response. All responses remain positive throughout the sample period but become insignificant in the late spring of 2020.

Similarly, the effects of COVID-19 case shocks on the CDS are found to be positive in all countries (see Fig. 4); however, they are significant only at the beginning of the pandemic and vary across countries. The highest response in terms of magnitude is observed for Spain, followed by the UK and the US, whilst the lowest impact of case shocks on the CDS is found for Italy. The highly contagious nature of COVID-19 led to a surge in the number of confirmed cases. Therefore, the government introduced several lockdown measures, which reduced economic activity and resulted in lower revenue and liquidity at the firm level. Further, access to financing dried up, reducing the probability of firms’ survival, and thus increasing default risk premia. This led to a greater probability of default and higher CDS. Positive CDS responses are consistent with the results of Andrieş et al. (2021), Daehler et al. (2021), Pan et al. (2021), and Augustin (2022) while partially confirming Yıldırım Karaman (2022). Similar to the findings of Cinicioglu (2023), CDS responses exhibit a time-varying pattern during the pandemic, and are found to be significant only in its early stages of the pandemic, consistently with the evidence reported by Cevik and Ozturkkal (2021). As Hao et al. (2022) and Havlik et al. (2022) showed, this may result from monetary and fiscal stimulus packages contributing to the decline in sovereign risk premia.

Regarding stock returns (see Fig. 5), significant negative responses are obtained for all countries, though the their timing and persistence vary across countries. The negative impact of COVID-19 cases on stock return lasted for a very short time in the US and France. This initial effect was also short-lived in Spain, although it reappeared in later periods. The responses are significant in the UK and Italy for a longer period, namely until August 2020 in the former and October 2020 in the latter. Germany is an exception, with a statistically significant adverse impact starting in July 2020 and lasting through mid-October 2020. Despite the results being to some extent mixed, it appears that the initial negative effect of COVID-19 cases on stock returns was short-lived in most countries.

The negative impact of COVID-19 cases on stock returns corroborates the findings of Al-Awadhi et al. (2020), Ashraf (2020a), Haroon and Rizvi (2020, Xu (2021), and Al-Quadah and Houcine (2022). Furthermore, our results are largely consistent with those of Capelle-Blancard and Desroziers (2020), Topcu and Gulal (2020), Anh and Gan (2021), and Harjoto and Rossi (2023), who reported that COVID-19 was no longer affecting stock markets by May 2020, and also confirm the conclusions of Guven et al. (2022), Ganie et al. (2022), and Yilmazkuday (2023), who found a weakening adverse impact of COVID-19 cases on stock returns.

There are various possible explanations for the observed rapid recovery of financial markets compared to real activity. First, the massive monetary expansion and fiscal stimulus packages announced at the national and international level since mid-March 2020 may have contributed to this rebound, as pointed out by Avalos and Xia (2020), Ashraf (2020b), Igan et al. (2020), Su (2020), Klose and Tillmann (2021), Chang et al. (2021), Narayan et al. (2021), Cortes et al. (2022), Aldhamari et al. (2023). Economic stimuli may have led to changes in investor sentiment, given the expectation that government intervention would improve market conditions. Second, containment measures to reduce the spread of the coronavirus may have improved stock market sentiment, with expectations becoming more optimistic (Guven et al. 2022; Saif-Alyousfi 2022). Finally, fear and anxiety about the pandemic may have raised the demand for precautionary saving, which drove up stock prices (Herrenbrueck 2021; Andre 2021).

Finally, we examine the time-varying responses of electricity consumption to COVID-19 case shocks (see Fig. 6). These are negative in all countries and only significant in the early stages of the pandemic. The largest impact of COVID-19 cases on economic activity is found in Italy and France. Fezzi and Fanghella (2020), who employed daily electricity consumption as a proxy for economic activity, had also documented an output loss of 30% of GDP in Italy during the first few months of the pandemic. Our findings are consistent with those of Fezzi and Fanghella (2020, 2021), Beyer et al. (2021), Ai et al. (2022), and Arshad and Beyer (2023), who reported that a decline in electricity consumption led to severe GDP losses, lockdowns and containment measures being the main causes.

Time-varying responses of electricity consumption to COVID-19 case shocks. a Time-varying cumulative responses. b Cumulative responses at h = 15 with \(\pm\) 2 standard error bands

In most countries in our sample, electricity consumption responses became insignificant by April and May 2020. This short-lived adverse impact is consistent with the evidence presented by Chen et al. (2020), who emphasized the role of easing restrictions, and Takyi et al. (2023), who stressed the contribution of governments’ economic support packages. Furthermore, the finding that the negative impact of cases on stock returns lasts longer than economic activity corroborates the results of Hasan et al. (2021).

5 Conclusions

This paper examines the effects of COVID-19 cases on stock returns, CDS, and economic activity in the US and the five European countries (the UK, Germany, France, Italy, and Spain) that have been most affected. The sample period covers the dates from 11 March 2020 to 19 February 2021. First, we estimated benchmark linear VAR models, and then, given the evidence of parameter instability, TVP-VAR models with stochastic volatility are also estimated to capture time-varying dynamics in the financial markets and the real economy (Primiceri 2005; Koop et al. 2009; Nakajima 2011).

The linear VAR responses of CDS to a one-standard-deviation shock to the number of COVID-19 cases are positive and statistically significant. The results for stock returns are mixed, whilst the electricity consumption responses are statistically insignificant. As for the TVP-VAR results, the COVID-19 cases had a positive influence on CDS at the beginning of the pandemic. Several measures and lockdowns reduced economic activity and resulted in lower revenue and liquidity. This led to rising stress on firms, whose access to finance dried up in an environment where economic stimuli had not been yet announced, and increased the default probability and CDS.

A significant adverse impact on stock markets is found in the early phases of the pandemic, except in Germany, and this effect gradually diminishes over the subsequent months. There are several explanations for this rebound. First, monetary expansion and fiscal stimulus packages not only increased income but also may have led to a change in investor sentiment concerning an improvement in market conditions. The other factor that may have contributed to more optimistic expectations is containment measures, which were introduced to reduce the spread of COVID-19. Finally, rising precautionary savings due to the fear of the pandemic may have been channelled into the stock market.

COVID-19 cases had a negative and significant effect on electricity consumption in all countries in the early stages of the pandemic (with cross-country differences). Lockdowns and stringency measures may have led to a sharp drop in economic activity while economic stimuli contributed to the recovery. The slump in stock returns occurred at the same time, which reflects the interaction between financial markets and the real sector.

The analysis carried out in this study has some limitations. First, our sample includes only the US and five European countries, namely only developed economies. It would also be worthwhile to obtain evidence concerning the emerging market economies, which are more vulnerable to external shocks. Second, our investigation was conducted at the aggregate level; additional insights could be gained by reproducing it at the sectoral level. Finally, country-specific factors accounting for differences in the responses of the variables of interest to the COVID-19 shock could be examined in greater depth. These issues are left for future research.

Notes

Baker et al. (2020) define a stock market jump as a situation when daily stock market movements are greater than \(\left| {2.5\% } \right|\).

Electricity consumption data are published every 15 min in Germany, every half hour in the UK, and every hour in the rest of the countries. This data is used to construct daily series. For instance, in the case of Germany, 96 observations have been collected for one day and divided by 24 to obtain the average hourly electricity consumption.

For a detailed survey of the literature on the nexus between electricity consumption and economic growth, see Payne (2010).

The data for European countries are available at.

https://transparency.entsoe.eu/load-domain/r2/totalLoadR2/show (Accessed: 21 February 2021).

The data for the US are obtained from https://www.eia.gov/opendata/qb.php?category=3389935&sdid=EBA.US48-ALL.D.H (Accessed: 21 February 2021).

Specifically, prior to the estimation, we examine the time series properties of the variables employing the Lumsdaine and Papell (1997) unit root test allowing for two structural breaks. The test statistics indicate that all series exhibit a unit root whilst their differences are stationary at the 1% significance level. Unit root test results are not reported but are available from the authors on request.

The random walk model is not stationary; hence we impose the stability restriction on the parameters as suggested by Cogley and Sargent (2005).

Using a geometric (exponential) random walk implies that the logarithm of the standard deviations follows a random walk.

To find the optimal number of lags, we used the Akaike Information Criterion (AIC). The same priors in Nakajima (2011) are employed in the TVP-VAR estimates.

The stability of the estimated TVP-VAR models investigated with the posterior means, standard deviations, and 95 percent confidence intervals of the chosen parameters can be inferred from Table 1 in the appendix. The convergence diagnostics (CD) by Geweke (1992) are low, and the posterior mean of the estimated parameters lies in the confidence intervals; in addition, the inefficiency factors imply that the null hypothesis of convergence to the posterior distribution is not rejected for any of the parameters of the models. Therefore, the diagnostic results confirm that the MCMC algorithm generates posterior draws efficiently. The CD test is used to evaluate the convergence of the Markov Chain in Bayesian models by comparing the first and last draws. If the MCMC sampling yields stable estimations, the posterior distribution of the parameters should converge to standard normal, and the null hypothesis of posterior distribution convergence cannot be rejected. Together with the CD test, we provide additional diagnostics in Fig. 8 for all countries' TVP-VAR models. These findings corroborate the posterior distribution's convergence. First, the chosen parameters' sample paths exhibit steady behavior since their autocorrelation functions rapidly converge to zero. Second, the shape of the distribution of the chosen parameters is near to the standard normal, as demonstrated by the CD test.

According to Nakajima (2011), time-varying responses are calculated by setting the initial shock magnitude identical to the average stochastic volatility over the estimation sample to make responses comparable over time.

References

Abu-Rayash A, Dincer I (2020) Analysis of the electricity demand trends amidst the COVID-19 coronavirus pandemic. Energy Res Soc Sci. https://doi.org/10.1016/j.erss.2020.101682

Aggarwal S, Nawn S, Dugar A (2021) What caused global stock market meltdown during the COVID pandemic-Lockdown stringency or investor panic? Finance Res Lett. https://doi.org/10.1016/j.frl.2020.101827

Aldhamari R, Ismail KNIK, Al-Sabri HMH, Saleh MSAH (2023) Stock market reactions of Malaysian firms and industries towards events surrounding COVID-19 announcements and number of confirmed cases. Pac Account Rev 35(3):390–411. https://doi.org/10.1108/PAR-08-2020-0125

Alomari M, Al Rababa’a AR, Rehman MU, Power DM (2022) Infectious diseases tracking and sectoral stock market returns: a quantile regression analysis. N Am J Econ 59:101584. https://doi.org/10.1016/j.najef.2021.101584

Al-Awadhi AM, Alsaifi K, Al-Awadhi A, Alhammadi S (2020) Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. J Behav Exp Finance. https://doi.org/10.1016/j.jbef.2020.100326

Al-Maadid A, Caporale GM, Spagnolo F, Spagnolo N (2021) Political tension and stock markets in the Arabian Peninsula. Int J Finance Econ 26(1):679–683. https://doi.org/10.1002/ijfe.1810

Al-Qudah A, Houcine A (2022) Stock markets’ reaction to COVID-19: evidence from the six WHO regions. J Econ Stud 49(2):274–289. https://doi.org/10.1108/JES-09-2020-0477

Ai H, Zhong T, Zhou Z (2022) The real economic costs of COVID-19: Insights from electricity consumption data in Hunan Province, China. Energy Econ. https://doi.org/10.1016/j.eneco.2021.1015747

Ambros M, Frenkel M, Huynh TLD, Kilinc M (2021) COVID-19 pandemic news and stock market reaction during the onset of the crisis: evidence from high-frequency data. Appl Econ Let 28(19):1686–1689. https://doi.org/10.1080/13504851.2020.1851643

Amin A, Arshad M, Sultana N, Raoof R (2022) Examination of impact of COVID-19 on stock market: evidence from American peninsula. J Econ Adm Sci 38(3):444–454. https://doi.org/10.1108/JEAS-07-2020-0127

Ampudia M, Baumann U, Fornari F (2020) Coronavirus (COVID-19): market fear as implied by options prices. ECB Econ Bull 4:51–55

André VC (2021) Rising Stocks during Lockdown Economic Recessions: Explaining the Phenomenon, MPRA Paper, 106710

Andrieş AM, Ongena S, Sprincean N (2021) The COVID-19 pandemic and sovereign bond risk. N Am J Econ Finance. https://doi.org/10.1016/j.najef.2021.101527

Angelov N, Waldenström D (2023) The impact of Covid-19 on economic activity: evidence from administrative tax registers. Int Tax Public Finance 30:1718–1746. https://doi.org/10.1007/s10797-023-09780-2

Anh DLT, Gan C (2021) The impact of the COVID-19 lockdown on stock market performance: evidence from Vietnam. J Econ Stud 48(4):836–851. https://doi.org/10.1108/JES-06-2020-0312

Arshad S, Beyer RCM (2023) Tracking economic fluctuations with electricity consumption in Bangladesh. Energy Econ. https://doi.org/10.1016/j.eneco.2023.106740

Ashraf BN (2020a) Stock markets’ reaction to COVID-19: Cases or fatalities? Res Int Bus Finance. https://doi.org/10.1016/j.ribaf.2020.101249

Ashraf BN (2020b) Economic impact of government interventions during the COVID-19 pandemic: international evidence from financial markets. J Behav Exp Finance. https://doi.org/10.1016/j.jbef.2020.100371

Augustin P, Sokolovski V, Subrahmanyam MG, Tomio D (2022) In sickness and in debt: The COVID-19 impact on sovereign credit risk. J Financ Econ 143(3):1251–1274. https://doi.org/10.1016/j.jfineco.2021.05.009

Avalos F, Xia D (2020) The short and long end of equity prices during the pandemic: Valuations and the shift in interest rates, BIS Q Rev, September, 9–10

Bahmanyar A, Estebsari A, Ernst D (2020) The impact of different COVID-19 containment measures on electricity consumption in Europe. Energy Res Soc Sci. https://doi.org/10.1016/j.erss.2020.101683

Baker SR, Bloom N, Davis SJ, Kost KJ, Sammon MC, Viratyosin T (2020) The unprecedented stock market impact of COVID-19. Rev Asset Pricing Stud 10(4):742–758. https://doi.org/10.1093/rapstu/raaa008

Bento PMR, Mariano SJPS, Calado MRA, Pombo JAN (2021) Impacts of the COVID-19 pandemic on electric energy load and pricing in the Iberian electricity market. Energy Rep. https://doi.org/10.1016/j.egyr.2021.06.058

Beyer RCM, Franco-Bedoya S, Galdo V (2021) Examining the economic impact of COVID-19 in India through daily electricity consumption and nighttime light intensity. World Dev. https://doi.org/10.1016/j.worlddev.2020.105287

Beyer RCM, Jain T, Sinha S (2023) Lights out? COVID-19 containment policies and economic activity. J Asian Econ. https://doi.org/10.1016/j.asieco.2023.101589

BIS (2020) BIS Quarterly Review: International banking and financial market developments, March

Capelle-Blancard G, Desroziers A (2020) The stock market is not the economy? Insights from the Covid-19 crisis, Covid Economics: Vetted and Real-Time Papers. CEPR Press, 28. June 12

Bover O, Fabra N, García-Uribe S, Lacuesta A, Ramos R (2023) Firms and households during the pandemic: what do we learn from their electricity consumption? Energy J 44(3):267–288. https://doi.org/10.5547/01956574.44.2.obov

Cairney P (2021) The UK government’s COVID-19 policy: assessing evidence-informed policy analysis in real time. Br Polit 16:90–116. https://doi.org/10.10157/s41293-020-00150-8

Carvalho V, Garcia JR, Hansen S, Ortiz Á, Rodrigo T, Mora JVR, Ruiz P (2021) Tracking the COVID-19 Crisis with high-resolution transaction data. R Soc Open Sci 8:210218. https://doi.org/10.1098/rsos.210218

Caporale GM, Çatık AN, Helmi MH, Ali FM, Tajik M (2020) The bank lending channel in the Malaysian Islamic and conventional banking system. Glob Finance J 45:100478. https://doi.org/10.1016/j.gfj.2019.100478

Cavallo E, Noy I (2011) Natural disasters and the economy—a survey. Int Rev Environ Res Econ 5(1):63–102. https://doi.org/10.1561/101.00000039

Cervantes P, Díaz A, Esparcia C, Huélamo D (2022) The impact of COVID-19 induced panic o stock market returns: a two-year experience. Econ Anal Policy. https://doi.org/10.1016/j.eap.2022.10.012

Cevik S, Öztürkkal B (2021) Contagion of fear: Is the impact of COVID-19 on sovereign risk really indiscriminate? Int Finance 24(2):134–154. https://doi.org/10.1111/infi.12397

Chang C-H, Feng G-F, Zheng M (2021) Government fighting pandemic, stock market return, and COVID-19 virus outbreak. Emerg Mark Finance Trade 57(8):2389–2406. https://doi.org/10.1080/1540496X.2021.1873129

Chau F, Deesomsak R, Wang J (2014) Political uncertainty and stock market volatility in the Middle East and North African (MENA) countries. J Int Financ Mark Inst Money 28:1–19. https://doi.org/10.1016/j.intfin.2013.10.008

Chen S, Igan D, Pierri N, Presbitero A F (2020) Tracking the Economic Impact of COVID-19 and Mitigation Policies in Europe and the United States, IMF Working Paper, 125

Chen H, Tillmann P (2023) Lockdown spillovers. J Int Money Finance. https://doi.org/10.1016/j.jimonfin.2023.102890

Chesney M, Reshetar G, Karaman M (2011) The impact of terrorism on financial markets: an empirical study. J Bank Finance 35(2):253–267. https://doi.org/10.1016/j.jbankfin.2010.07.026

Chundakkadan R, Nedumparambil E (2021) In search of COVID-19 and stock market behavior. Glob Finance J. https://doi.org/10.1016/j.gfj.2021.100639

Cinicioglu EN, Huyugüzel Kışla G, Önder AÖ, Muradoğlu YG (2023) The changing behavior of the European credit default swap spreads during the covid-19 pandemic: a bayesian network analysis. Comput Econ. https://doi.org/10.1007/s10614-023-10489-x

Cogley T, Sargent TJ (2005) Drifts and volatilities: monetary policies and outcomes in the post WWII US. Rev Econ Dyn 8(2):262–302. https://doi.org/10.1016/j.red.2004.10.009

Cortes GS, Gao GP, Silva FB, Song Z (2022) Unconventional monetary policy and disaster risk: evidence from the subprime and COVID–19 crises. J Int Money Finance. https://doi.org/10.1016/j.jimonfin.2021.102543

Daehler TB, Aizenman J, Jinjarak Y (2021) Emerging markets sovereign CDS spreads during COVID-19: economics versus epidemiology news. Econ Model. https://doi.org/10.1016/j.econmod.2021.105504

Deb P, Furceri D, Ostry JD, Tawk N (2022) The economic effects of COVID-19 containment measures. Open Econ Rev 33:1–32. https://doi.org/10.1007/s11079-021-09638-2

D'Orazio P, Dirks M W (2020) COVID-19 and financial markets: Assessing the impact of the coronavirus on the Eurozone. Ruhr Economic Papers, 859

Eichenbaum MS, Rebelo S, Trabandt M (2021) The macroeconomics of epidemics. Rev Financ Stud 34(11):5149–5187. https://doi.org/10.1093/rfs/hhab040

Elsayed AH, Helmi MH (2021) Volatility transmission and spillover dynamics across financial markets: the role of geopolitical risk. Ann Oper Res 305:1–22. https://doi.org/10.1007/s10479-021-04081-5

Fezzi C, Fanghella V (2020) Real-time estimation of the short-run impact of COVID-19 on economic activity using electricity market data. Environ Resour Econ 76:885–900. https://doi.org/10.1007/s10640-020-00467-4

Fezzi C, Fanghella V (2021) Tracking GDP in real-time using electricity market data: insights from the first wave of COVID-19 across Europe. Eur Econ Rev. https://doi.org/10.1016/j.euroecorev.2021.103907

FSB (2020) COVID-19 pandemic: financial stability implications and policy measures taken, April 15

Furceri D, Kothari S, Zhang L (2021) The effects of COVID-19 containment measures on the Asia-Pacific region. Pac Econ Rev 26:469–497. https://doi.org/10.1111/1468-0106.12369

Gagnon JE, Kamin SB, Kearns J (2023) The impact of the COVID-19 pandemic on global GDP growth. J Jpn Int Econ. https://doi.org/10.1016/j.jjie.2023.101258

Galdi G, Casarin R, Ferrari D, Fezzi C, Ravazzolo F (2023) Nowcasting industrial production using linear and non-linear models of electricity demand. Energy Econ 126:107006. https://doi.org/10.1016/j.eneco.2023.107006

Ganie IR, Wani TA, Yadav MP (2022) Impact of COVID-19 outbreak on the stock market: an evidence from selected countries. Bus Perspect Res. https://doi.org/10.1177/22785337211073635

Gaskell J, Stoker G, Jennings W, Devine D (2020) Covid-19 and the blunders of our governments: long-run system failings aggravated by political choices. Polit Q 91(3):523–533. https://doi.org/10.1111/1467-923X.12894

Geweke J (1992) Evaluating the accuracy of sampling-based approaches to the calculation of posterior moments. In: Bernardo JM, Berger JO, Dawid AP, Smith AFM (eds) Bayesian statistics, 4. Oxford University Press, Oxford, pp 169–193

Gopinath G (2020) The great lockdown: worst economic downturn since the great depression. IMF Blog 14:2020

Guven M, Cetinguc B, Guloglu B, Calisir F (2022) The effects of daily growth in COVID-19 deaths, cases, and governments’ response policies on stock markets of emerging economies. Res Int Bus Finance. https://doi.org/10.1016/j.ribaf.2022.101659

Hale T, Angrist N, Goldszmidt R, Kira B, Petherick A, Phillips T, Webster S, Cameron-Blake E, Hallas L, Majumdar S, Tatlow H (2021) A global panel database of pandemic policies (Oxford COVID-19 Government Response Tracker). Nat Hum Behav 5:529–538. https://doi.org/10.1038/s41562-021-01079-8

Hao X, Sun Q, Xie F (2022) The COVID-19 pandemic, consumption and sovereign credit risk: cross-country evidence. Econ Model. https://doi.org/10.1016/j.econmod.2022.105794

Harjoto MA, Rossi F (2023) Market reaction to the COVID-19 pandemic: evidence from emerging markets. Int J Emerg Mark 18(1):173–199. https://doi.org/10.1108/IJOEM-05-2020-0545

Haroon O, Rizvi SAR (2020) Flatten the curve and stock market liquidity – inquiry into emerging economies. Emerg Mark Finance Trade 56(10):2151–2161. https://doi.org/10.1080/1540496X.2020.1784716

Hasan MB, Mahi M, Sarker T, Amin MR (2021) Spillovers of the COVID-19 pandemic: Impact on global economic activity, the stock market, and the energy sector. J Risk Financ Manag 14(5):200. https://doi.org/10.3390/jrfm14050200

Havlik A, Heinemann F, Helbig S, Nover J (2022) Dispelling the shadow of fiscal dominance? Fiscal and monetary announcement effects for euro area sovereign spreads in the corona pandemic. J Int Money Finance. https://doi.org/10.1016/j.jimonfin.2021.102578

Herrenbrueck L (2021) Why a pandemic recession boosts asset prices. J Math Econ. https://doi.org/10.1016/j.jmateco.2021.102491

Horvath R (2021) Natural catastrophes and financial depth: An empirical analysis. J Financial Stab. https://doi.org/10.1016/j.jfs.2021.100842

Igan D, Kirti D, Peria S M (2020) The Disconnect between Financial Markets and the Real Economy, IMF Special Notes Series on COVID-19. https://www.imf.org/en/Publications/SPROLLs/covid19-special-notes

IMF (2020) Global Financial Stability Report: Markets in the Time of COVID-19, April

Ji X, Bu N, Zheng C, Xiao H, Liu C, Chen X, Wang K (2024) Stock market reaction to the COVID-19 pandemic: an event study. Portuguese Econ J 23:167–186. https://doi.org/10.1007/s10258-022-00227-w

Janzen B, Radulescu D (2020) Electricity use as a real-time indicator of the economic burden of the COVID-19-related lockdown: evidence from Switzerland. Cesifo Econ Stud 66(4):303–321. https://doi.org/10.1093/cesifo/ifaa010

Janzen B, Radulescu D (2022) Effects of COVID-19 related government response stringency and support policies: Evidence from European firms. Econ Anal Policy 76:129–145. https://doi.org/10.1016/j.eap.2022.07.013

Kanno M (2024) Assessing the impact of the COVID-19 crisis on sovereign default risk. Res Int Bus Finance. https://doi.org/10.1016/j.ribaf.2023.102198

Klose J, Tillmann P (2021) COVID-19 and financial markets: a panel analysis for european countries. J Econ Stat 241(3):297–347. https://doi.org/10.1515/jbnst-2020-0063

Klose J, Tillmann P (2023) Stock market response to Covid-19, containment measures and stabilization policies-The case of Europe. Int Econ 173:29–44. https://doi.org/10.1016/j.inteco.2022.11.004

Kok JLC (2020) Short-term trade-off between stringency and economic growth, Covid economics: vetted and real-time papers. CEPR Press 60(4):172–189

Koop G, Leon-Gonzales R, Strachan R (2009) On the evolution of the monetary policy transmission mechanism. J Econ Dyn Control 33(4):997–1017. https://doi.org/10.1016/j.jedc.2008.11.003

Lazo J, Aguirre G, Watts D (2022) An impact study of COVID-19 on the electricity sector: a comprehensive literature review and Ibero-American survey. Renew Sustain Energy Rev. https://doi.org/10.1016/j.rser.2022.112135

Lewis D, Mertens K, Stock JH, Trivedi M (2022) Measuring real activity using a weekly economic index. J Appl Econ 37(4):667–687. https://doi.org/10.1002/jae.2873

Lumsdaine RL, Papell DH (1997) Multiple trend breaks and the unit-root hypothesis. Rev Econ Stat 79(2):212–218. https://doi.org/10.1162/003465397556791

Ma L, Zhang C, Lo KL, Meng X (2023) Can stringent government initiatives lead to global economic recovery rapidly during the COVID-19 epidemic. Int J Environ Res Public Health. https://doi.org/10.3390/ijerph20064993

Matei I (2023) Assessing the impact of pandemic measures on economic growth in a globalizing world: a non-linear panel. Anal Appl Econ. https://doi.org/10.1080/00036846.2023.2296371

Menezes F, Figer V, Jardim F, Medeiros P (2022) A near real-time economic activity tracker for the Brazilian economy during the COVID-19 pandemic. Econ Model. https://doi.org/10.1016/j.econmod.2022.105851

Nakajima J (2011) Time-varying parameter VAR model with stochastic volatility: an overview of methodology and empirical applications. Monet Econ Stud 29:107–142

Nakajima J, Watanabe T (2011) Bayesian analysis of time-varying parameter vector autoregressive model with the ordering of variables for the Japanese economy and monetary policy. Global COE Hi-Stat Discussion Paper Series, 196

Narayan PK, Narayan S, Prasad A (2008) A structural VAR analysis of electricity consumption and real GDP: Evidence from the G7 countries. Energy Policy 36:2765–2769. https://doi.org/10.1016/j.enpol.2008.02.027

Narayan PK, Phan DHB, Liu G (2021) COVID-19 lockdowns, stimulus packages, travel bans, and stock returns. Finance Res Lett. https://doi.org/10.1016/j.frl.2020.101732

Pan W-F, Wang X, Wu G, Xu W (2021) The COVID-19 pandemic and sovereign credit risk. China Financial Rev Int 11(3):287–301. https://doi.org/10.1108/CFRI-01-2021-0010

Payne JE (2010) A survey of the electricity consumption-growth literature. Appl Energy 87:723–731. https://doi.org/10.1016/j.apenergy.2009.06.034

Phan DHB, Narayan PK, Gong Q (2021) Terrorist attacks and oil prices: Hypothesis and empirical evidence. Int Rev Financ Anal. https://doi.org/10.1016/j.irfa.2021.101669

Primiceri GE (2005) Time-varying structural vector autoregressions and monetary policy. Rev Econ Stud 72(3):821–852. https://doi.org/10.1111/j.1467-937X.2005.00353.x

Refinitiv Eikon Datastream, 2021. Refinitiv. https://www.refinitiv.com/en/products/datastream-macroeconomic-analysis Accessed February 28 2021

Roth F, Jonung L, Most A (2024) COVID-19 and public support for the Euro. Empirica 51:61–86. https://doi.org/10.1007/s10663-023-09596-7

Pham TTX, Chu TTT (2024) Covid-19 severity, government responses and stock market reactions: a study of 14 highly affected countries. J Risk Finance 25(1):130–159. https://doi.org/10.1108/JRF-04-2023-0085

Saif-Alyousfi AYH (2022) The impact of COVID-19 and the stringency of government policy responses on stock market returns worldwide. J Chin Econ Foreign Trade Stud 15(1):87–105. https://doi.org/10.1108/JCEFTS-07-2021-0030

Santiago I, Moreno-Munoz A, Quintero-Jimenez P, Garcia-Torres F, Gonzalez-Redondo J (2021) Electricity demand during pandemic times: the case of the COVID-19 in Spain. Energy Policy. https://doi.org/10.1016/j.enpol.2020.111964

Sarwar S, Chen W, Waheed R (2017) Electricity consumption, oil price and economic growth: global perspective. Renew Sustain Energy Rev 76:9–18. https://doi.org/10.1016/j.rser.2017.03.063

Sánchez-López M, Moreno R, Alvarado D, Suazo-Martínez C, Negrete-Pincetic M, Olivares D, Sepúlveda C, Otárola H, Basso LJ (2022) The diverse impacts of COVID-19 on electricity demand: The case of Chile. Int J Electr Power Energy Syst. https://doi.org/10.1016/j.ijepes.2021.107883

Scherf M, Matschke X, Rieger MO (2022) Stock market reactions to COVID-19 lockdown: a global analysis. Finance Res Lett. https://doi.org/10.1016/j.frl.2021.102245

Sharif A, Aloui C, Yarovaya L (2020) COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: fresh evidence from the wavelet-based approach. Int Rev Financial Anal. https://doi.org/10.1016/j.irfa.2020.101496

Shephard N, Pitt MK (1997) Likelihood analysis of non-Gaussian measurement time series. Biometrika 84(3):653–667

Sims CA, Zha T (2006) Were there regime switches in US monetary policy? Am Econ Rev 96(1):54–81. https://doi.org/10.1257/000282806776157678

Stock J, Watson M (1998) A Comparison of Linear and Nonlinear Univariate Models for Forecasting Macroeconomic Time Series (No. 6607). National Bureau of Economic Research, Inc

Szczygielski JJ, Charteris A, Bwanya PR, Brzeszczyński J (2022) The impact and role of COVID-19 uncertainty: A global industry analysis. Int Rev Financial Anal. https://doi.org/10.1016/j.irfa.2021.101837

Su E (2020) Why Have Stock Market and Real Economy Diverged During the COVID-19 Pandemic? Congressional Research Service Reports. https://www.everycrsreport.com/reports/IN11494.html

Takyi PO, Dramani JB, Akosah NK, Aawaar G (2023) Economic activities’ response to the COVID-19 pandemic in developing countries. Sci Afr 20: e01642. https://doi.org/10.1016/j.sciaf.2023.e01642

Topcu M, Gulal OS (2020) The impact of COVID-19 on emerging stock markets. Finance Res Lett. https://doi.org/10.1016/j.frl.2020.101691

Wang Q, Li S, Jiang F (2021) Uncovering the impact of the COVID-19 pandemic on energy consumption: new insight from difference between pandemic-free scenario and actual electricity consumption in China. J Clean Prod. https://doi.org/10.1016/j.jclepro.2021.127897

Watanabe T, Omori Y (2004) A multi-move sampler for estimating non-Gaussian time series models: Comments on Shephard & Pitt (1997). Biometrika 91(1):246–248

Wen L, Sharp B, Suomalainen K, Sheng MS, Guang F (2022) The impact of COVID-19 containment measures on changes in electricity demand. Sustain Energy Grids Netw. https://doi.org/10.1016/j.segan.2021.100571

WHO (2020a) WHO Director-General’s statement on IHR Emergency Committee on Novel Coronavirus (2019-nCoV). https://www.who.int/ Accessed February 25 2021

WHO (2020b) WHO Director-General’s opening remarks at the media briefing on COVID-19 – March 11 2020. https://www.who.int/ Accessed February 25 2021

WHO (2021) WHO Coronavirus Disease (COVID-19) Dashboard. https://covid19.who.int/ Accessed February 25 2021

WHO (2023) WHO Director-General’s opening remarks at the media briefing – May 5 2023. https://www.who.int/ Accessed January 12 2024

World Bank (2021) Global Economic Prospects, January

Xu L (2021) Stock return and the COVID-19 pandemic: evidence from Canada and the US. Finance Res Lett. https://doi.org/10.1016/j.frl.2020.101872

Yıldırım Karaman S (2022) Covid-19, sovereign risk and monetary policy: evidence from the European Monetary Union. Central Bank Rev 22:99–107. https://doi.org/10.1016/j.cbrev.2022.08.001

Yilmazkuday H (2023) COVID-19 effects on the S&P 500 index. Appl Econ Lett 30(1):7–13. https://doi.org/10.1080/13504851.2021.1971607

Yoo S-H, Kwak S-Y (2010) Electricity consumption and economic growth in seven South American countries. Energy Policy 38:181–188. https://doi.org/10.1016/j.enpol.2009.09.003

Yukseltan E, Kok A, Yucekaya A, Bilge A, Aktunc EA, Hekimoglu M (2022) The impact of the COVID-19 pandemic and behavioral restrictions on electricity consumption and the daily demand curve in Turkey. Util Pol 76:101359. https://doi.org/10.1016/j.jup.2022.101359

Zou Q, Wang Y, Modi S (2024) Linking government interventions to firm performance: the influence of stringency and support during the COVID-19 pandemic. Int J Oper Prod Manag 44(2):393–423. https://doi.org/10.1108/IJOPM-01-2023-0032

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible Editor: Jesus Crespo Cuaresma.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Caporale, G.M., Çatık, A.N., Helmi, M.H. et al. Time-varying effects of the COVID-19 pandemic on stock markets and economic activity: evidence from the US and Europe. Empirica 51, 529–558 (2024). https://doi.org/10.1007/s10663-024-09608-0

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10663-024-09608-0