Abstract

Low-carbon road freight transport is pivotal in mitigating global warming. Nonetheless, electrifying heavy-duty vehicles poses a tremendous challenge due to high technical requirements and cost competitiveness. Data on future truck costs are scarce and uncertain, complicating assessments of the future role of zero-emission truck (ZET) technologies. Here we derive most likely cost developments for price setting ZET components by meta forecasting from more than 200 original sources. We find that costs are primed to decline much faster than expected, with significant differences between scientific and near-market estimates. Specifically, battery system costs could drop by 64% to 75% and fall below €150 kWh−1 by no later than 2035, whereas fuel cell system costs may exhibit even higher cost reductions but are unlikely to reach €100 kW−1 before the early 2040s. This fast cost decline supports an optimistic view on the ZET market diffusion and has substantial implications for future energy and transport systems.

Similar content being viewed by others

Main

The fast electrification of heavy road freight transport is pivotal in limiting global warming in line with the Paris Climate Agreement1,2,3. This follows since heavy-duty vehicles (HDVs) contribute a noteworthy proportion of annual greenhouse gas emissions despite a low share in the vehicle stock4. Whereas the European Union has agreed on ambitious tail-pipe emissions reduction targets for newly sold HDVs of −43% by 2030, −65% by 2035 and −90% by 2040 (compared with 2019/2020)5, California has effectively imposed the phase out of conventional combustion trucks by 20366, with other US states expected to follow. Similarly, China is anticipated to tighten its tail-pipe emissions reduction targets soon to comply with its near-zero emissions target by 20607,8. These ambitions require the fast deployment of zero-emission trucks (ZETs), where demand from and, hence, affordability for operators are key. However, high acquisition costs are currently hampering fast ZET market diffusion9,10,11,12,13. This culminates in an active and cross-national debate between industry, politics and academia about different measures and technological pathways of how to decarbonize HDVs1,14,15,16,17,18,19, particularly about the respective roles of battery-electric trucks (BETs) and fuel cell trucks (FCETs) in future ZET fleets.

Although many studies have explored cost-reduction potentials using qualitative or quantitative methods20,21, such as literature-based projections, expert elicitation, detailed cost breakdowns or learning and experience curves, results are limited to the respective application category and system configuration22,23. For example, studies emphasizing private passenger car electrification have shown that costs for key components such as batteries are expected to fall substantially and quickly24,25,26, with increasing evidence that battery-electric vehicles will constitute the primary technology1,27. However, electrifying heavy commercial trucks, such as US Class 7/8 or European N2/N3, still poses a tremendous challenge, particularly due to altered requirements limiting the transferability of passenger car findings. This can be ascribed to inherently versatile operating characteristics from urban delivery to international long haul, distinct utilization schedules, versatile value-adding duties from cargo transport to ancillary power- or energy-intensive services, greater lifetime mileage even beyond 1 million km, high reliability and longevity and an even more pronounced cost sensitivity13,16,18,28. Hence, accurate and comprehensive data on current and projected ZET acquisition costs are essential to assess the future roles of these technologies. However, data are scarce and heterogeneous, whereas a holistic overview assessing multiple components for heavy ZETs within a consistent scope and comparative method is missing. Thus, we address the following research question: what are the most likely future cost developments of central ZET components until 2050?

This paper analyses projected costs for five crucial BET and/or FCET components based on an extensive literature record: whereas we find limited cost reductions for the three adjacent components (that is, electric traction motors, power electronics and high-voltage system (PE&HV) components and hydrogen tanks), costs for battery and fuel cell (FC) systems are primed to decline much faster than expected and due in course. Despite inevitable uncertainty, a rapid ZET market diffusion associated with ambitious learning rates (LRs) at the required breakthrough costs seems within reach soon. Yet, prospects for BETs as primary technology seem more favourable at higher confidence, with faster availability and achieving cost effectiveness as of today, thus supporting an optimistic view on the fast decarbonization of road freight transport.

Meta forecast using regression analysis

Meta forecasting involves synthesizing existing projections from literature encompassing historical trends, future expectations and different methods to yield novel ones. Pooling individual forecasts through this well-established approach29,30 enhances accuracy, often outperforming individual forecasts31.

We identified relevant literature via distinct search strings using the Scopus and Google Scholar databases. Following Nykvist and Nilsson25, we considered three different source categories: near market (that is, market outlooks from renowned analysts and consultancies and industry announcements), scientific (that is, peer-reviewed papers) and others (that is, non-peer-reviewed academic publications and reports). All cost values were harmonized to represent system-level original equipment manufacturer (OEM) purchase prices for the respective ZET component, including profit mark-ups (+35%) and specified in 2020 euros (€2020). Component-specific cost developments were calculated by regression of log harmonized cost data and log time data using either weighted least squares (WLS) or ordinary least squares (OLS). Herein we controlled for several auxiliary variables such as release dates, scenario settings, data originality, forecast method and source category. Additionally, we used three robust approaches to strengthen our results by reducing potential outliers’ contribution (Methods).

Rapidly declining battery system and fuel cell system costs

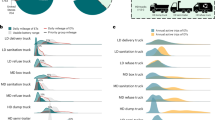

Figure 1 illustrates that battery system costs, broken down by source categories, may decline by 64% to 75% until 2050. We observe rapid and consistent cost reductions per annum (p.a.), with similar patterns for all source categories. We find cost reductions (CRs) of around 5% p.a. (scientific and others) to 6.5% p.a. (near market) until 2030 and 3.3–4.5% p.a. over an extended 2020–2050 period. Notably, near-market estimates (blue) are more optimistic, less heterogeneous and more stable compared with the other categories. This consolidates into expected cost estimates, where near-market estimates project a decrease from around €2020275 kWh−1 in 2020 to €2020140 kWh−1 by 2030 and around €202070 kWh−1 by 2050. In contrast, scientific estimates (green) indicate a drop from roughly €2020310 kWh−1 in 2020 to €2020180 kWh−1 by 2030 and around €2020100 kWh−1 by 2050. Other estimates (purple) also project more conservative progress, cutting €2020200 kWh−1 by 2030 and approximating €2020115 kWh−1 by 2050. The cross-category projection (black) closely aligns with scientific projections.

System-level costs per kWh of total gross battery capacity. These include, among others, battery and thermal management systems, cell modules, housing, connectors, wiring and assembly. Black circle markers represent the original harmonized data. Solid lines represent the regression results (log–log, WLS, mean values), with the shaded areas (that is, error bars) in the zoom-level plot (period 2020–2050) as 95% confidence intervals (mean ± 2 s.e.m.). The source category is colour coded: near market in blue (analysts, consultancies, industry announcements), scientific in green (peer-reviewed papers) and others in purple (non-peer-reviewed academic publications). Total results (that is, cross-category) in black. The total sample covers N = 1,104 data points from 200 unique studies. Cross-category R² is 0.49. The figure legend states the number of data points (N) and the R² values per source category. Additional information is available in Supplementary Tables 1 and 4.

Figure 2 illustrates that FC system costs, broken down by source categories, may decline by 65% to 85% until 2050. Notably, our observations unveil significant heterogeneity among these categories. Near-market estimates (blue) initiate at approximately €2020540 kW−1 in 2020, undercut the €2020100 kW−1 threshold by 2045 and attain around €202085 kW−1 by 2050. This equals CRs of around 9% p.a. until 2030 and around 6% p.a. over 2020–2050. Conversely, scientific estimates (green) initiate at approximately €2020 kW−1 in 2020 and fall below €2020100 kW−1 in the late 2030s, ultimately reaching around €202080 kW−1 by 2050 and CRs of around 3.5% p.a. over 2020–2050. Other estimates (purple) are centred between near-market and scientific estimates without reaching sub-€2020100 kW−1 levels.

System-level costs per kW of rated power. These include, among others, control systems, thermal management, housing, hydrogen supply except for storage, air intake, including compressor and humidifier and assembly. Black circle markers represent the original harmonized data. Solid lines represent the regression results (log–log, WLS, mean values), with the shaded areas (that is, error bars) in the zoom-level plot (period 2020–2050) as 95% confidence intervals (mean ± 2 s.e.m.). The source category is colour coded: near market (blue: analysts, consultancies, industry announcements), scientific (green: peer-reviewed papers) and others (purple: non-peer-reviewed academic publications). Total results (that is, cross-category) in black. The total sample size covers N = 424 data points from 83 unique studies. Cross-category R² is 0.33. The figure legend states the number of data points (N) and the R² values per source category. Additional information is available in Supplementary Tables 1 and 4.

Cost overview for five major ZET components

Table 1 shows the derived heavy ZET component costs (mean ± two standard errors). Unlike for battery and FC costs, we find less substantial CR potentials for the adjacent ZET components using the same method, albeit with smaller samples and less detail (Supplementary Figs. 14–17). Precisely, costs for electric motors probably fall from around €202042 kW−1 by 2020 to €202030 kW−1 by 2050 (−1.2% p.a.). For hydrogen tanks, we find CRs of around 2.6–2.9% p.a. over 2020–2050. This translates into decreasing system costs from around €202017 kWh−1 (liquid-LH2) and €202024 kWh−1 (compressed-CH2) by 2020 to around €20207 kWh−1 (LH2) and €202011 kWh−1 (CH2) by 2050. Last, we derive stable system costs of around €202050 kW−1 for PE&HV components.

Different cost expectations for batteries and fuel cells

Our meta forecasts project a rapid cost decline for both batteries and FCs, while we disclose a contrasting dynamic that highlights the complex interplay between scientific projections and tangible market realities for emerging technologies at different stages of commercial maturity.

Our analysis of battery cost predictions unveils that near-market estimates are remarkably stable over different release dates. These projections are prone to only minor downward adjustments, as indicated by the difference between OLS and WLS results (Supplementary Figs. 5 and 6 and Supplementary Table 2), and are consistently more optimistic than those from scientific literature (p < 0.05, two-tailed t-test; Supplementary Table 4). Conversely, scientific cost estimates published in 2010–2023 faced substantial downward adjustments. Hence, battery costs have experienced a more rapid decline than initially expected, at least in the scientific community. This echoes Nykvist and Nilsson25, who found similar divergences for industry vs market leaders vs peer-reviewed literature estimates and supports conclusions from Frith et al.32, who emphasize substantial gaps between academic and industry perspectives. One explanation might be that near-market sources may have more practical in-depth knowledge about technologies, manufacturing or cost-saving measures and better access to industry insights such as market trends, partnerships, supply chain dynamics or confidential pricing data. In contrast, parts of the scientific literature may be classified as theoretical estimates or may be affected by citation patterns or time-delaying review processes, leading to the self-confirmation of outdated values and assumptions.

However, FC system costs exhibit an inverse trend. Scientific estimates show higher stability and are consistently more optimistic (p < 0.05, two-tailed t-test; Supplementary Table 5) than near-market estimates.

One explanation for these different dynamics might be the technological maturity of both technologies and the related uncertainty about future pathways. The lower spread and consistency across all source categories for battery system costs may indicate higher confidence and technological readiness, as BETs are increasingly projected to inherit a pivotal role in future road freight transport1—at least on short to medium distances—and have been announced in the portfolios of all major truck OEMs27,33. In contrast, the future role of FCETs and their development from laboratory to market is still more uncertain, resulting in larger data spread and potentially conservative projections from near-market sources.

Required volumes, learning rates and breakthrough costs

Whereas cumulative production volumes may be the best-performing predictor of theoretical technology cost compared with others22,34, findings are hard to generalize into policy decisions and anticipated timescales. In parallel, the underlying data and thus observed cost estimates implicitly assume a certain relevance of battery technology and fuel cells for future road freight transport or even other sectors. This relevance may be expressed as growing cumulative investments, economies of scale, supply chain improvements, spill-over effects and material or production improvements that would not occur without this relevance. Hence, we compare our cost estimates against the potential S-shaped market diffusion of ZETs in North America, Europe and China, totalling around 2.5–3 million trucks produced p.a. (Methods and Supplementary Figs. 12 and 13).

To achieve battery system costs of approximately €2020150 kWh−1 as indicated by our regression to be achievable between 2028 (near market) and 2032 (scientific), cumulative production volumes must range from 1,300 GWh (near market) to 5,200 GWh (scientific). This yields short-term compound annual growth rates (CAGRs) of 39–49%. Those volumes may be feasible in the early 2030s if BETs take large market shares fast, given their head start in the early 2020s. Corresponding LRs would be around 16% (scientific) to 19% (near market). Falling below €2020100 kWh−1, as indicated by our regression to be achievable between 2039 (near market) and 2049 (scientific), would require up to 11,000 GWh (near market) or even 68,000 GWh (scientific), with the former being probably feasible within the late 2030s given that BETs comprise substantial market shares and long-term CAGRs of 25–29%.

Considering breakthrough levels, Teichert et al.35 find system costs of €2020120–200 kWh−1 to reach cost parity with current diesel trucks if fast charging becomes available. This confirms Nykvist and Olsson19, who state around €2020200 kWh−1 as the upper threshold. Basma et al.36 specify system costs of around €2020100 kWh−1 as viable tipping point for European BETs to become cost effective, even without policy support through purchase incentives, adjusted road toll schemes or CO2 pricing. For the United States, Phadke et al.37 quantify system costs below US$135 kWh−1, confirming Sripad and Viswanathan38, who quantified the Tesla Semi case to be economically viable well below US$150 kWh−1.

Similarly, to attain fuel cell system costs of approximately €2020150 kW−1, as our regression suggests between 2027 (scientific) and 2035 (near market), cumulative production volumes span from 135,000 units (scientific) to 1.4 million units (near market). The latter appears attainable, considering the broader availability of FCET models anticipated to emerge in the late 2020s1, with short-term CAGRs of 35–46%. Corresponding LRs would be around 14% (scientific) to 26% (near market). Falling below €2020100 kW−1, as indicated by our regression to be achievable between 2040 (scientific) and 2045 (near market), would then demand cumulative volumes from 2.3 million (scientific) to 6.8 million units (near market) and long-term CAGRs of 26–29%.

Our ambitious LRs align with other technologies, with Nykvist and Nilsson25 suggesting conceivable LRs for batteries of 12–14%, and Schmidt et al.22 finding LRs of 9–18% for electrical energy storage technologies. Similarly, historical growth rates for wind and solar capacity were at least 15% and often 39–50% (ref. 39), whereas general technology adoption growth rates were often below 13–14% but selectively exceeded 30–40% (ref. 40). For BEVs, sales growth ranged around 25–55% (Supplementary Table 7), with Norway achieving nearly 90% BEV sales within 13 years (CAGR2010–2023 = 41.4%), compared with Europe’s 25% share (CAGR2010–2023 = 28.1%).

Discussion

Over-extrapolation and theoretical assessments may result in deceptive conclusions of future performance and relevance, which is critical for public and private funding and, hence, policy decisions32. Therefore, we contrast our findings to target or floor costs—typically defined by raw material and production costs—to avoid excessively low-cost estimates22,34,41.

Recalibrating our battery system costs to the cell level (Supplementary Table 6), we arrive at around €202090 kWh−1 by 2030 or €202070 kWh−1 by 2050. Several facts underpin the feasibility of the derived costs despite potential non-negligible disruptions caused by raw material shortages, supply chain disruptions, higher inflation levels, increased energy costs or raw material shortages42,43,44, whereof the latter’s effect would depend on the specific chemistry. Calculated system- and cell-level costs do not fall below original scientific or near-market estimates and announced industry values, as could have happened by the regression. For example, the European Battery Strategic Research and Innovation Agenda (SRIA)45 targets system costs of around €202075 kWh−1 by 2025 and even below by 2030 and beyond. Plus, Tesla confirmed cell-level cost targets for its 4,680 cylindrical cells of around US$70 kWh−1 at their third quarter Earning Call in 2022—even before US incentive programmes such as the Inflation Reduction Act. The projected ready-to-drive prime costs of the first generation 500-mile Tesla Semi truck, equipped with these cells and suspected 800–900 kWh, stand at roughly US$200,000 in 202346, indicating associated battery system costs below US$150 kWh−1. However, we also address potential strategies for gaining initial market shares by internally subsidizing battery packs.

For fuel cell system costs, the US Department of Energy ultimately targets HDV FC system costs of around US$201680 kW−1 by 2030 and US$201660 kW−1 by 205047, with both targets adopted by numerous studies. Similarly, the European hydrogen SRIA48 targets system costs of below €100 kW−1 by 2030. This indicates a notable level of ambition or required federal support but might also mean that our projections (specified as OEM purchase price) may be quite optimistic and close to anticipated floor and target costs.

Our cost-centred meta forecast focuses on most likely developments and consistent comparisons, potentially omitting scenario dependencies and technical particularities/trends.

Underlying scenarios and assumptions, such as different mitigation pathways, can impact production volumes and, thus, component cost developments. However, insufficient standardized scenario classifications and missing congruent information impede robust and consistent cross-study assessments. Further regressions indicate that optimistic cost scenarios imply additional cost benefits for batteries and FCs (Supplementary Tables 4 and 5).

The current effects of technical designs and material choices on costs and performance are well documented24,49, with pre-series and commercial components disclosing real-world pricing or facilitating cost versus performance trade-off analyses35 and product tear downs50,51. However, exact technical designs, materials and properties of next-generation components until 2050 are theoretical, remain highly uncertain and are only selectively available. This impedes comprehensive techno-economic assessments for single technologies across 2020–2050.

Whereas cost reductions and increased technical performance are anticipated for batteries52,53 and FCs47,48, our stable results for PE&HV and minor savings for electric motors indicate that technical advancements involving new components and trends may offset cost reductions. This may involve advancements54,55 to increase efficiency and thus driving range per charge, such as transitioning to higher voltage, new motor topologies and materials or bidirectional system architectures to facilitate Vehicle-to-Grid (V2G) applications.

Concerning data limitations and potential bias, we state that our data sample is very recent, with most sources being published between 2018 and 2022 (Supplementary Fig. 1). Whereas we consider our findings regarding battery system costs as highly robust, we acknowledge uncertainty for FC system costs.

The battery dataset, comprising N = 200 sources, displays a balanced representation across all categories of sources, encompassing various methods and scenarios employed therein. Consequently, we have not identified either substantial bias originating from the data sample or issues from the data harmonization (Supplementary Figs. 2–4 and 11 and Supplementary Table 4).

The FC data sample consists N = 83 sources and exhibits an imbalance towards other sources, particularly limited upon near-market estimates, limiting the significance of cross-category outcomes. Our findings indicate that methods and scenario considerations exert more pronounced effects on the results. Furthermore, the impact of data harmonization is more accentuated, with harmonized values being lower than the original ones, indicating cost developments are too low (15–25%) (Supplementary Figs. 2–4 and 11 and Supplementary Table 5).

Three approaches using two techniques, namely robust norms and outlier removal, strengthened the validity of our original regression results. Precisely, HuberT regression, RANSAC regression and WLS regression with only the central 50% or 80% of observations within five-year time windows yield future costs close to or within our original prediction errors (Supplementary Figs. 7–10 and Supplementary Table 3).

For both battery and fuel cell data, and similar to Schmidt et al.22, we find that more recent sources embed faster and larger cost-reduction potentials, expressed by the difference between OLS and WLS results (Supplementary Figs. 5 and 6 and Supplementary Table 2).

Total Cost of Ownership (TCO) benefits against diesel trucks (DTs) typically constitute the key ZET criterion for fleet operators9,10,11,12,13, with other factors being also relevant. Using a recent TCO framework56 along with our cost projections, we find that BETs may realize cost benefits versus DTs as of today. In contrast, FCETs may struggle to reach TCO parity throughout the 2030s because green hydrogen prices remain probably too high. Herein the share of acquisition costs substantially rises for ZETs compared with current DTs, whereas energy storage size, energy prices and mileage are the most sensitive parameters (Methods and Supplementary Figs. 18 and 19).

Alongside economic considerations, technical capabilities such as feasible range, realizable payload, reliability, ageing behaviour and recharging/refuelling times are further influencing factors on truck purchase decisions. Several studies indicate that current and announced ZETs are already close to become technically competitive with DTs19,35,49,57. Finally, infrastructure availability and user acceptance will be decisive9,10,11,12,13.

Conclusion

This article presents a systematic overview of cost estimates for five major ZET components with meta forecasting and regression analysis. We draw four conclusions from this analysis.

First, we show that ZET component costs are likely to decline substantially and in due course. Precisely, future battery system costs are more robust, likely to fall below €2020150 kWh−1 by no later than 2035, and to approach or even cross €2020100 kWh−1 upon 2050, with the former corresponding to typical expected breakthrough levels. FC system costs are likely to reach around €2020150 kW−1 in the late 2030s and to approach €2020100 kW−1 at best in the late 2040s, with lower values close to target and floor cost values warranting careful consideration. We emphasize that calculated LRs, cost reductions and growth rates are challenging to reach, but similar ranges have been witnessed for (energy) technologies in the past22,39,40, with similar to higher scales for FC values.

Second, we find that cost predictions differ systematically between different source categories, potentially depending on technological maturity. Whereas near-market sources turn to be the most stable source for batteries, their predictions are more optimistic than those from scientific sources. However, the opposite is true for fuel cells, with the scientific sources being more optimistic and often close to floor or target costs.

Third, these substantial and fast cost-reduction potentials support an optimistic outlook for both technologies. This indicates rapid ZET market deployments that will substantially impact transportation and energy sector players, such as value chain reconfigurations, establishing national and international hydrogen ecosystems and electricity infrastructure expansions from transformers to distribution and transmission grids.

Finally, we highlight the competition among ZET technologies, raising questions about market leadership and whether we need different technologies. All anticipated cost reductions rely on successful transitions to low-carbon road freight transport. This entails building large-scale production facilities supported by policy measures in key markets like North America, Europe and China, particularly in the early market phases. These measures may include purchase subsidies, infrastructure development, ZET mandates and carbon pricing. This policy support may phase out later when the technology has matured and costs have decreased. Our TCO indicates that BETs may constitute the most cost-effective pathway in reaching TCO parity with less policy support needed, in contrast to FCETs, which might require more policy support throughout the 2030s.

Methods

Literature identification

We identified the relevant academic literature via distinct search strings using the Scopus and Google Scholar databases and complemented the identified studies with commercial market outlooks from renowned analysts and consultancies and industry announcements. Table 2 presents the search strategy, which has been used on article titles, abstracts and keywords published between 2010 and May 2023. Available literature has then been analysed and filtered based on the abstracts. The final sample for batteries covered NB = 200 sources and DPB = 1,104 data points. The final sample for fuel cells covered NFC = 83 sources and DPFC = 424 data points.

Literature parameters

We collected available auxiliary data from each source to either harmonize the data or integrate those parameters as control variables in the regression analysis to compare and validate the results: (1) value type, differentiating between cost or price, with the latter typically including additional overheads, mark-ups, indirect costs or supplier profits. However, we denote that both terms are also used synonymously. (2) Application type, differentiating between automotive- or HDV-certified values, as altered requirements and scales also lead to different configurations, designs and costs. (3) Currency and (4) reference year information were collected to ensure accurate contextualization and temporal accuracy. (5) Scenario information was collected, differentiating between low (mass-market), high (niche market) and medium. (6) Forecast method, differentiating between literature-based projections, expert elicitation, detailed bottom-up cost modelling or learning and experience curves. (7) Data originality, differentiating between original or adopted values. (8) Integration level, differentiating between cell- or system-level values for batteries and stack- or system-level values for fuel cells. This raw data are available for download, yet proprietary is anonymized.

Literature classification

In addition to the parameters stated above, all sources have been classified into three categories to further differentiate results (similar to Nykvist and Nilsson25). Accordingly, we differentiated between scientific (literature) covering peer-reviewed papers and PhD theses. Others involved non-peer-reviewed academic publications such as conference articles, reports, working or white papers and book contributions. Near market involved market outlooks from renowned analysts or consultancies and industry announcements.

Data harmonization

Data harmonization, based on the upper parameters, ensured that all data points were specified as system-level OEM purchase prices in €2020 for the respective component. Initially, this involved (3) currency conversions based on the respective historical exchange rate (subject to the reference year or release date) and (4) inflation adjustment to 2020 levels (annual mean over all member states of the European Union (EU-27) issued by the European Commission and downloadable via Eurostat). Potential inhomogeneities caused by (1) cost or price type, (2) application type or (8) integration level are harmonized based on studies that explicitly state multiple values differentiated according to (1), (2), (8). Hence, all cost values were topped with a 35% surcharge (median value from battery data as no temporal trend could be identified) to derive OEM purchase prices. Scaling automotive-certified components to HDV-certified ones, data showed a temporal trend for batteries but not for fuel cells. Hence, we used a decreasing scaling factor for batteries from around 80% in 2020 to 50% in 2030 and 20% in 2050, indicating higher integration, potential enhancements through on-purpose designs and usable synergies. For fuel cells, all automotive-type values were topped with a 100% surcharge (median value). For cell-to-system or stack-to-system scaling, data showed a clear temporal trend for both batteries and fuel cells. Therefore, we used a decreasing scaling for batteries from around 40% in 2020 to 30% in 2030 and 20% in 2050. In contrast, we used an increasing scaling factor for fuel cells from 60% in 2020 to 90% in 2030 and 125% in 2050, meaning that the cost share of the actual stacks on total system costs was expected to decrease. Supplementary Figs. 2–4 provide more details. These harmonized data are available for download.

Regression analysis and control variables

Results were calculated by regression using Python statsmodels. Specifically, we used the log harmonized cost data and log time data to approximate the typical learning curve shape and controlled for several auxiliary variables stated above. Weighting (WLS) was performed by source age using the following exponential function for smoothing, as proposed by refs. 58,59:

Robust approaches

We used two robust techniques, namely robust norms and outlier removal, in three approaches to exclude outliers and noise, thus increasing the accuracy and robustness of our original regression results. First, we performed HuberT regression analyses that are less sensitive to outliers by minimizing a combined loss function of squared errors for small residuals and absolute errors for larger residuals but still using the full data sample. Second, we filtered the data by labelling the central 50% (that is, values within the lower and upper quartile) and 80% (that is, values within the 10% and 90% quantile) of observations as inliers and others as outliers. We then performed a WLS regression with inliers only. Third, we performed a RANSAC (Random Sample Consensus) regression that iteratively selects random data subsets to fit a regression model, identifies inliers based on a predetermined threshold (that is, median absolute deviation), refits the model using these inliers and selects the best model (that is, regression coefficients) based on the minimum absolute error. Supplementary Figs. 7–10 provide further details and Supplementary Table 3 provides model comparison.

TCO framework

We adopted the total cost of ownership (TCO) framework (that is, calculation and parameter assumptions, excluding component costs) from Noll et al.56 to calculate TCO per kilometre (€ km−1) over the whole vehicle service life. This includes capital expenditures such as truck purchase (Supplementary Note 1) and resale and operating expenditures, such as energy costs, road tolls, maintenance and service. The capital recovery factor discounts future payments using a specific discount rate. We excluded any subsidy or purchase price premiums for ZETs, averaged all parameters at a European level and tested our results against various energy prices and annual vehicle mileages. Supplementary Figs. 18 and 19 and Supplementary Table 8 provide more details.

Cumulative volumes and learning rates

We used S-shaped diffusion curves (sigmoid functions) to obtain potential BET/FCET shares per year, using the following function:

where yt (%) is the annual BET/FCET share in a particular year, S (%) is the total annual market capacity (= 100%), y0 (%) is the initial share for the starting year and k is the growth rate. This share is then multiplied by the combined North American, European and greater China HDV production volume of around 2.5 million–3 million units per year to derive annual volumes. Following the announced or expected ZET sales shares for those regions, we assume most new trucks will have zero emissions by 2040 to 2050 (y2040 > 90% and y2050 = 100%) in Europe and North America, whereas greater China will reach this threshold later (y2060 = 100%). This leads to annual growth rates between around 25% (China) and 40% (Europe and North America). We assume the same isolated market diffusion for both technologies—BET and FCET—to guarantee comparability, and we ignore any other ZET technology. The average BET battery capacity was assumed to increase from 300 kWh in 2018 to 500 kWh in 2025 and 600 kWh from 2030 onwards. The cumulative volume (in GWh) is calculated by multiplying the battery capacity and annual volumes. Initial sales/production data on BETs and FCETs were then matched to respective reference years (\(\left.{{{y}}}_{2018},\ldots ,{{{y}}}_{2022}\right)\), which allowed calculation of learning rates by regression of log cost data and log cumulative volumes. Supplementary Figs. 12 and 13 provide more details.

Data availability

All fuel cell and battery data presented in this study (that is, raw and harmonized datasets) are publicly available and can be found in the attached Supplementary Information. However, for raw data files, proprietary data from commercial sources, such as purchased market studies, cannot be published and corresponding records are anonymized. Data for other components are available upon request. Source data are provided with this paper.

Code availability

The Python model (OLS and WLS regression, robust regression and visualization for Figs. 1 and 2) is available in the attached Supplementary Information. Reproduced figures or regression results based on the raw data files may not involve any proprietary data leading to changes compared with the original results and plots in this paper.

Change history

26 June 2024

In the version of this article initially published, there was a typo in the units discussed in the second to last sentence, which is now amended in the HTML and PDF versions of the article.

References

Jaramillo, P. et al. in IPCC, 2022 - Climate Change 2022: Mitigation of Climate Change (eds Shukla, P. R. et al.) Ch. 10 (Cambridge Univ. Press, 2023).

Plötz, P. et al. Greenhouse gas emission budgets and policies for zero-carbon road transport in Europe. Clim. Policy 23, 343–354 (2023).

Creutzig, F. et al. Energy and environment. Transport: a roadblock to climate change mitigation? Science 350, 911–912 (2015).

Tracking Clean Energy Progress 2023 https://www.iea.org/reports/tracking-clean-energy-progress-2023 (IEA, 2023).

Heavy-duty Vehicles: Council and Parliament Reach a Deal to Lower CO2 Emissions from Trucks, Buses and Trailers https://www.consilium.europa.eu/en/press/press-releases/2024/01/18/heavy-duty-vehicles-council-and-parliament-reach-a-deal-to-lower-co2-emissions-from-trucks-buses-and-trailers (European Council, 2024).

California Approves World’s First Regulation to Phase Out Dirty Combustion Trucks and Protect Public Health https://www.gov.ca.gov/2023/04/28/california-approves-worlds-first-regulation-to-phase-out-dirty-combustion-trucks-and-protect-public-health/ (Office of Gov. Gavin Newsom, 2023).

Zhang, Y. & Hui, H. China’s efforts to decarbonize road transport: decent, but not sufficient. ICCT https://theicct.org/china-ev-efforts-mar22 (2023).

Khanna, N., Lu, H., Fridley, D. & Zhou, N. Near and long-term perspectives on strategies to decarbonize China’s heavy-duty trucks through 2050. Sci. Rep. 11, 20414 (2021).

Anderhofstadt, B. & Spinler, S. Factors affecting the purchasing decision and operation of alternative fuel-powered heavy-duty trucks in Germany—a Delphi study. Transp. Res. Part D Transp. Environ. 73, 87–107 (2019).

Bae, Y., Mitra, S. K., Rindt, C. R. & Ritchie, S. G. Factors influencing alternative fuel adoption decisions in heavy-duty vehicle fleets. Transp. Res. Part D Transp. Environ. 102, 103150 (2022).

Ragon, P.-L. & Rodríguez, F. Road Freight Decarbonization in Europe. Readiness of the European Fleets for Zero-emission Trucking https://theicct.org/wp-content/uploads/2022/09/road-freight-decarbonization-europe-sep22.pdf (ICCT, 2022).

Spiller, B., Lohawala, N. & DeAngeli, E. Medium- and Heavy-Duty Vehicle Electrification: Challenges, Policy Solutions, and Open Research Questions https://media.rff.org/documents/Report_23-03_v3.pdf (RFF, 2023).

Muratori, M., Borlaug, B., Ledna, C., Jadun, P. & Kailas, A. Road to zero: research and industry perspectives on zero-emission commercial vehicles. iScience 26, 106751 (2023).

Plötz, P. Hydrogen technology is unlikely to play a major role in sustainable road transport. Nat. Electron. 5, 8–10 (2022).

Why the battery electric drive represents the future for trucks. Traton https://traton.com/en/newsroom/current-topics/why-the-battery-electric-drive-represents-the-future-for-trucks.html (2022).

Staffell, I. et al. The role of hydrogen and fuel cells in the global energy system. Energy Environ. Sci. 12, 463–491 (2019).

Meyer, T. Decarbonizing road freight transportation—a bibliometric and network analysis. Transp. Res. Part D Transp. Environ. 89, 102619 (2020).

Borlaug, B. et al. Heavy-duty truck electrification and the impacts of depot charging on electricity distribution systems. Nat. Energy 6, 673–682 (2021).

Nykvist, B. & Olsson, O. The feasibility of heavy battery electric trucks. Joule 5, 901–913 (2021).

Niazi, A., Dai, J. S., Balabani, S. & Seneviratne, L. Product cost estimation: technique classification and methodology review. J. Manuf. Sci. Eng. 128, 563–575 (2006).

Farmer, J. D. & Lafond, F. How predictable is technological progress? Res. Policy 45, 647–665 (2016).

Schmidt, O., Hawkes, A., Gambhir, A. & Staffell, I. The future cost of electrical energy storage based on experience rates. Nat. Energy https://doi.org/10.1038/nenergy.2017.110 (2017).

Luo, X., Wang, J., Dooner, M. & Clarke, J. Overview of current development in electrical energy storage technologies and the application potential in power system operation. Appl. Energy 137, 511–536 (2015).

Schmuch, R., Wagner, R., Hörpel, G., Placke, T. & Winter, M. Performance and cost of materials for lithium-based rechargeable automotive batteries. Nat. Energy 3, 267–278 (2018).

Nykvist, B. & Nilsson, M. Rapidly falling costs of battery packs for electric vehicles. Nat. Clim. Change 5, 329–332 (2015).

Mauler, L., Duffner, F., Zeier, W. G. & Leker, J. Battery cost forecasting: a review of methods and results with an outlook to 2050. Energy Environ. Sci. 14, 4712–4739 (2021).

IEA. Global EV Outlook 2023. Catching Up With Climate Ambitions (IEA, 2023).

Becker, H. et al. Preparing the World for Zero-emission Trucks. The Mainstays of Commercial Road Transport Will Soon Benefit from Cost-effective, Zero-emission Horsepower (McKinsey & Co., 2022).

Atiya, A. F. Why does forecast combination work so well? Int. J. Forecasting 36, 197–200 (2020).

Clemen, R. T. Combining forecasts: a review and annotated bibliography. Int. J. Forecasting 5, 559–583 (1989).

Timmermann, A. Chapter 4 forecast combinations. Handb. Econ. Forecasting 1, 135–196 (2006).

Frith, J. T., Lacey, M. J. & Ulissi, U. A non-academic perspective on the future of lithium-based batteries. Nat. Commun. 14, 420 (2023).

Drive to zero’s zero-emission technology inventory (ZETI). Tool version 8.0. CALSTART https://globaldrivetozero.org/tools/zero-emission-technology-inventory/ (2022).

Junginger, M. Technological Learning in the Transition to a Low-Carbon Energy System. Conceptual Issues, Empirical Findings, and Use in Energy Modeling (Elsevier Science & Technology, 2020).

Teichert, O., Link, S., Schneider, J., Wolff, S. & Lienkamp, M. Techno-economic cell selection for battery-electric long-haul trucks. eTransportation 16, 100225 (2023).

Basma, H., Saboori, A. & Rodríguez, F. Total Cost of Ownership for Tractor-trailers in Europe: Battery-electric Versus Diesel https://theicct.org/wp-content/uploads/2021/11/tco-bets-europe-1-nov21.pdf (ICCT, 2021).

Phadke, A., Khandekar, A., Abhyankar, N., Wooley, D. & Rajagopal, D. Why Regional and Long-Haul Trucks are Primed for Electrification Now (LBNL, 2021).

Sripad, S. & Viswanathan, V. Quantifying the economic case for electric semi-trucks. ACS Energy Lett. 4, 149–155 (2019).

Odenweller, A., Ueckerdt, F., Nemet, G. F., Jensterle, M. & Luderer, G. Probabilistic feasibility space of scaling up green hydrogen supply. Nat Energy 7, 854–865 (2022).

Nemet, G., Greene, J., Müller-Hansen, F. & Minx, J. C. Dataset on the adoption of historical technologies informs the scale-up of emerging carbon dioxide removal measures. Commun. Earth Environ. 4, 397 (2023).

Hsieh, I.-Y. L., Pan, M. S., Chiang, Y.-M. & Green, W. H. Learning only buys you so much: practical limits on battery price reduction. Appl. Energy 239, 218–224 (2019).

Mauler, L., Lou, X., Duffner, F. & Leker, J. Technological innovation vs. tightening raw material markets: falling battery costs put at risk. Energy Adv. 1, 136–145 (2022).

BloombergNEF’s annual battery price survey 2022. Lithium-ion battery pack prices rise for first time to an average of $151/kWh. BloombergNEF https://about.bnef.com/blog/lithium-ion-battery-pack-prices-rise-for-first-time-to-an-average-of-151-kwh (2022).

The Lithium-Ion (EV) Battery Market and Supply Chain. Market Drivers and Emerging Supply Chain Risks https://content.rolandberger.com/hubfs/07_presse/Roland%20Berger_The%20Lithium-Ion%20Battery%20Market%20and%20Supply%20Chain_2022_final.pdf (Roland Berger, 2022).

Strategic Research and Innovation Agenda https://bepassociation.eu/wp-content/uploads/2021/09/BATT4EU_reportA4_SRIA_V15_September.pdf (BATT4EU, 2021).

Kane, M. Elon Musk confirms Tesla Semi will enter the market later this year. InsideEVs https://insideevs.com/news/603515/tesla-semi-deliveries-later-this-year/ (2022).

Marcinkoski, J. et al. DOE Advanced Truck Technologies. Subsection of the Electrified Powertrain Roadmap—Technical Targets for Hydrogen-Fueled Long-Haul Tractor-Trailer Trucks https://www.hydrogen.energy.gov/docs/hydrogenprogramlibraries/pdfs/19006_hydrogen_class8_long_haul_truck_targets.pdf?Status=Master (DOE, 2019).

Strategic Research and Innovation Agenda 2021–2027 Annex to GB decision number CleanHydrogen-GB-2022-02 https://www.clean-hydrogen.europa.eu/about-us/key-documents/strategic-research-and-innovation-agenda_en (Clean Hydrogen Partnership, 2022).

Cullen, D. A. et al. New roads and challenges for fuel cells in heavy-duty transportation. Nat. Energy 6, 462–474 (2021).

Günter, F. J. & Wassiliadis, N. State of the art of lithium-ion pouch cells in automotive applications: cell teardown and characterization. J. Electrochem. Soc. 169, 30515 (2022).

Ank, M. et al. Lithium-ion cells in automotive applications: Tesla 4680 cylindrical cell teardown and characterization. J. Electrochem. Soc. 170, 120536 (2023).

Gao, Y., Pan, Z., Sun, J., Liu, Z. & Wang, J. High-energy batteries: beyond lithium-ion and their long road to commercialisation. Nano-Micro Lett. 14, 94 (2022).

Battery Requirements for Future Automotive Applications https://eucar.be/wp-content/uploads/2019/08/20190710-EG-BEV-FCEV-Battery-requirements-FINAL.pdf (EUCAR, 2019).

Cai, W., Wu, X., Zhou, M., Liang, Y. & Wang, Y. Review and development of electric motor systems and electric powertrains for new energy vehicles. Automot. Innov. 4, 3–22 (2021).

Husain, I. et al. Electric Drive Technology Trends, Challenges, and Opportunities for Future Electric Vehicles (ORNL, 2021).

Noll, B., Del Val, S., Schmidt, T. S. & Steffen, B. Analyzing the competitiveness of low-carbon drive-technologies in road-freight: a total cost of ownership analysis in Europe. Appl. Energy 306, 118079 (2022).

Mauler, L., Dahrendorf, L., Duffner, F., Winter, M. & Leker, J. Cost-effective technology choice in a decarbonized and diversified long-haul truck transportation sector: a US case study. J. Energy Storage 46, 103891 (2022).

Hyndman, R. J. & Athanasopoulos, G. in Forecasting: Principles and Practice 2nd edn Ch. 7 (OTexts, 2018).

Guthrie, W. F. e-Handbook of Statistical Methods Ch. 6.4.3 http://www.itl.nist.gov/div898/handbook/ (NIST, 2020).

Acknowledgements

We gratefully acknowledge funding from the EU STORM project (grant number 101006700: P.P., D.S., S.L.) by the European Union’s Horizon 2020 research and innovation programme, the HoLa project (FKZ 03EMF0404A: P.P., D.S., S.L.) by the German Federal Ministry for Digital and Transport and the BEMA project (FKZ 03XP0272B: S.L., A.S.) by the German Federal Ministry for Education and Research. We thank M. Wietschel and H. Döscher for their comments and discussions and S. Lange (all Fraunhofer ISI) for English editing.

Funding

Open access funding provided by Fraunhofer-Gesellschaft zur Förderung der angewandten Forschung e.V.

Author information

Authors and Affiliations

Contributions

S.L. conceived and designed the study in consultation with P.P. and A.S. S.L. collected the data, implemented the model and created the visualizations. S.L. wrote the original manuscript with contributions from all co-authors. In particular, P.P. and A.S. contributed to the discussion, interpretation of findings, recommendations and policy implications. D.S. edited the paper and contributed to the data collection. P.P. supervised the study.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Nature Energy thanks Heikki Liimatainen, Mehdi Jahangir Samet and the other, anonymous, reviewer(s) for their contribution to the peer review of this work.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Supplementary Information

Supplemental Figs. 1–19, Tables 1–8, Note 1 and references.

Source data

Source Data Fig. 1

Harmonized data for system-level OEM purchase prices for heavy-duty truck batteries.

Source Data Fig. 2

Harmonized data for system-level OEM purchase prices for heavy-duty truck fuel cells.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Link, S., Stephan, A., Speth, D. et al. Rapidly declining costs of truck batteries and fuel cells enable large-scale road freight electrification. Nat Energy 9, 1032–1039 (2024). https://doi.org/10.1038/s41560-024-01531-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1038/s41560-024-01531-9

- Springer Nature Limited